Florida, the Sunshine State, is a dream destination for many. Whether you’re planning a sun-drenched escape to the beaches of Miami, a family adventure at Walt Disney World, or a business trip to the bustling metropolis of Orlando, driving is often the most convenient way to explore. However, before you hit the open road and embark on your Florida travel adventures, understanding the state’s car insurance requirements is paramount. This guide will delve into Florida’s compulsory insurance laws, the types of coverage you need, and how it impacts your accommodation and lifestyle choices when visiting or residing in this vibrant state.

Understanding Florida’s Minimum Insurance Requirements

Florida operates under a “no-fault” insurance system. This means that regardless of who is at fault in an accident, your own insurance policy will cover your medical expenses and lost wages up to a certain limit. This system is designed to expedite the claims process and reduce the number of lawsuits filed after minor collisions.

Personal Injury Protection (PIP)

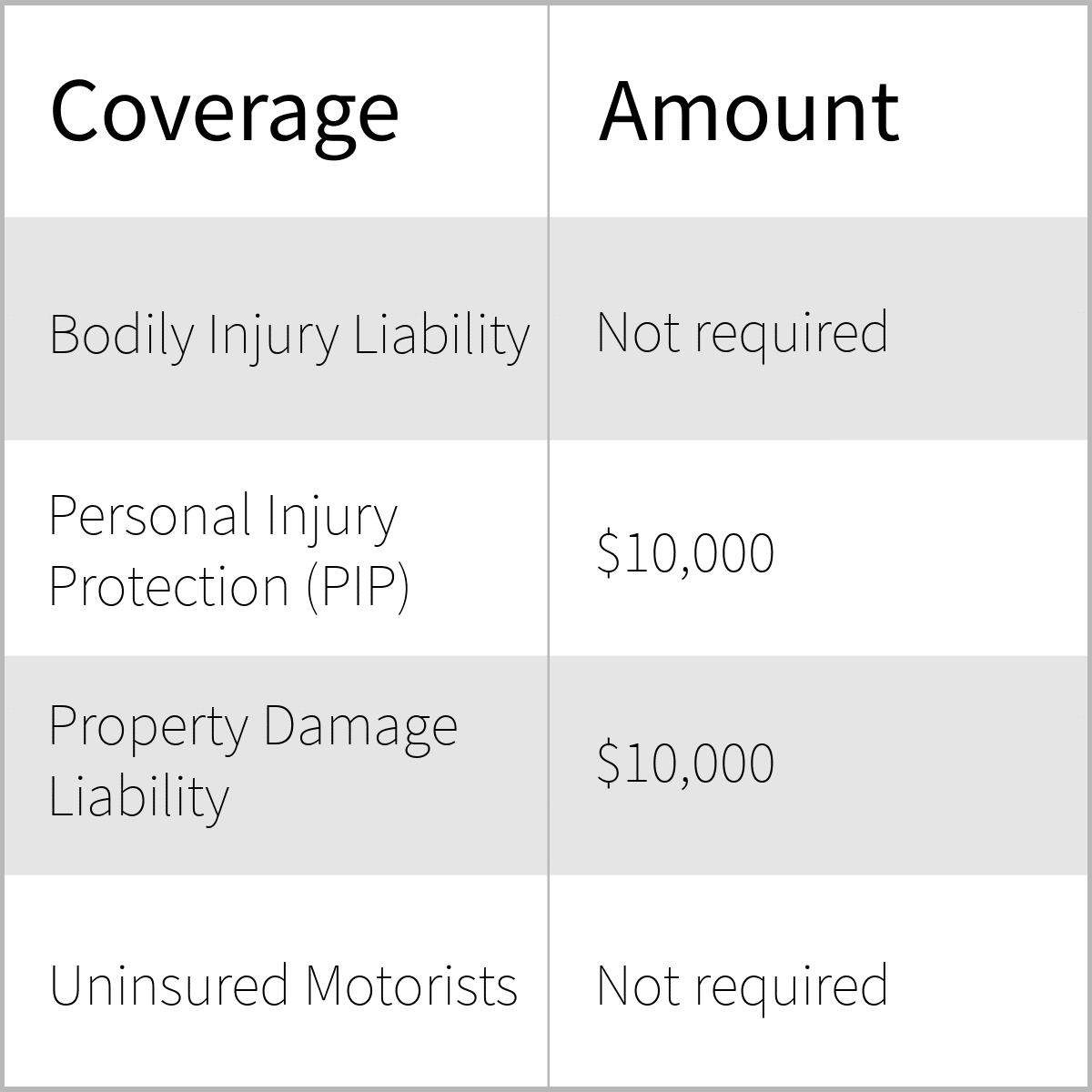

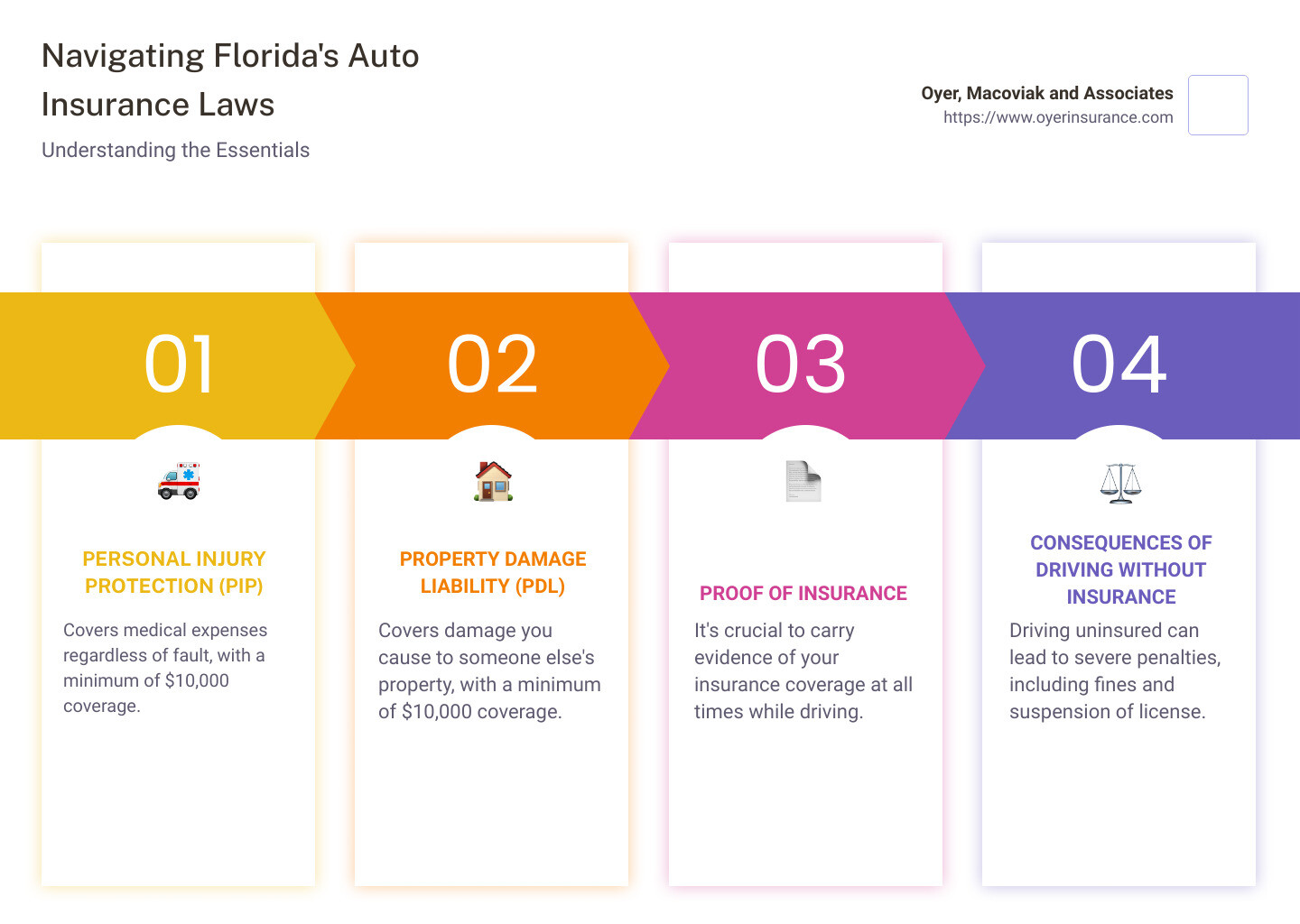

The cornerstone of Florida’s no-fault system is Personal Injury Protection (PIP) coverage. This is a mandatory component of your auto insurance policy if you own a vehicle registered in Florida or if you are a resident who drives in the state. PIP is designed to cover a percentage of your medical bills and 60% of your lost wages, regardless of who caused the accident.

- Medical Expenses: PIP typically covers 80% of your medical expenses resulting from a car accident, up to a specified limit. This can include hospital stays, doctor’s visits, surgery, and rehabilitation.

- Lost Wages: As mentioned, PIP covers 60% of your lost income due to injuries sustained in an accident. This can be a crucial lifeline if you are unable to work for a period.

- Death Benefits: In the unfortunate event of a fatality, PIP also includes a death benefit, which can help cover funeral expenses and provide some financial support to your dependents.

The minimum PIP coverage required by Florida law is $10,000. However, it’s important to understand that this is a minimum. Many insurance providers offer higher levels of PIP coverage, which can provide greater financial protection in the event of a serious accident.

Property Damage Liability (PDL)

In addition to PIP, Florida law also mandates Property Damage Liability (PDL) coverage. This coverage is essential for protecting others from the financial burden of damages to their property caused by your negligence.

- Vehicle Damage: PDL covers the cost of repairing or replacing the other party’s vehicle if you are found to be at fault in an accident.

- Other Property: This coverage also extends to damage to other types of property, such as fences, buildings, or other structures that you may impact during an accident.

The minimum PDL coverage required by Florida law is $10,000 per accident. Again, this is a baseline, and opting for higher coverage limits is strongly recommended to ensure adequate protection against potentially significant repair or replacement costs.

Bodily Injury Liability (BIL)

While Florida’s no-fault system emphasizes covering your own medical expenses through PIP, it is crucial to understand that PIP has limitations. If your medical expenses exceed your PIP coverage, or if you cause an accident that results in severe injuries to others, Bodily Injury Liability (BIL) coverage becomes vital.

While not strictly mandated as a minimum requirement for all drivers in the same way as PIP and PDL, if you are determined to be at fault for an accident that causes bodily injury to another person, you will be held financially responsible for their medical expenses and other damages. This is where BIL coverage is essential.

Many financial experts and insurance professionals strongly advise carrying BIL coverage to protect yourself from potentially devastating financial liabilities. The minimum liability limits often discussed in conjunction with Florida’s laws are typically:

- $10,000 for bodily injury per person.

- $20,000 for bodily injury per accident.

- $10,000 for property damage per accident.

These are often referred to as “10/20/10” limits. However, these are often considered low in today’s economic climate. A serious accident could easily result in medical bills far exceeding these amounts, leaving you personally liable for the difference.

Liability for Serious Injury or Fatality

The no-fault system has specific thresholds under which a driver can be sued for damages beyond their PIP coverage. These thresholds are typically met when an accident results in:

- Significant and permanent injury: This can include injuries like broken bones, disfigurement, or loss of a bodily function.

- Permanent impairment: A substantial loss of use of a body part or function.

- Death: The most severe outcome, where a lawsuit for wrongful death can be filed.

In these situations, if you are found to be at fault, you could be liable for significant medical expenses, lost earning capacity, pain and suffering, and other damages. This is precisely why Bodily Injury Liability (BIL) coverage is so important. It acts as a financial shield, protecting your assets from being depleted by lawsuits arising from severe accidents.

Implications for Visitors and New Residents

The car insurance requirements in Florida are not just for long-term residents; they also have significant implications for visitors and those planning to relocate.

Visitors Driving in Florida

If you are visiting Florida and plan to drive a vehicle, you must ensure you have adequate insurance coverage.

- Renting a Car: Rental car companies in Florida are required to provide vehicles that meet the state’s minimum insurance requirements. However, the coverage included in the rental price may be the bare minimum. It is highly recommended to purchase supplemental insurance from the rental agency or to ensure your personal auto insurance policy provides adequate coverage for rental vehicles. This is particularly important for tourism and travel where you might be venturing to various attractions and landmarks across the state.

- Driving Your Own Vehicle: If you are driving your own vehicle into Florida, your insurance policy from your home state or country should comply with Florida’s minimum requirements. If your policy offers less coverage than Florida mandates, you may be operating illegally. It is advisable to contact your insurance provider before your trip to confirm your coverage meets or exceeds Florida’s standards.

New Residents

If you are moving to Florida, you have a grace period to switch your car insurance to a Florida-compliant policy.

- Vehicle Registration: To register your vehicle in Florida, you will need proof of Florida insurance. This typically means obtaining a Florida PIP and PDL policy.

- Driver’s License: Similarly, when applying for a Florida driver’s license, you will need to demonstrate financial responsibility, which includes having the required insurance. The Florida Department of Highway Safety and Motor Vehicles oversees these requirements.

Failing to maintain the required insurance can lead to severe penalties, including license suspension, vehicle impoundment, and fines.

Beyond the Minimum: Recommendations for Comprehensive Coverage

While Florida law mandates minimum levels of PIP and PDL, relying solely on these minimums can leave you financially vulnerable in the event of a serious accident. Considering the state’s busy roads, especially around popular tourist destinations like Orlando, Miami, and the Florida Keys, and the potential for costly repairs and medical bills, investing in more comprehensive coverage is a wise decision.

Collision and Comprehensive Coverage

- Collision Coverage: This coverage helps pay for damage to your own vehicle if it is involved in a collision with another vehicle or object, regardless of fault. This is especially important if you own a newer or more valuable car.

- Comprehensive Coverage: This covers damage to your vehicle from events other than collisions, such as theft, vandalism, fire, falling objects, or natural disasters like hurricanes, which are a significant concern in Florida.

Uninsured/Underinsured Motorist (UM/UIM) Coverage

This is a critical, though often overlooked, type of coverage. Many drivers in Florida operate with the bare minimum insurance, and some unfortunately drive uninsured altogether.

- Uninsured Motorist (UM): If you are involved in an accident with a driver who has no insurance, UM coverage will step in to cover your medical expenses and, in some cases, property damage.

- Underinsured Motorist (UIM): If you are involved in an accident with a driver whose insurance limits are too low to cover the full extent of your damages, UIM coverage will cover the difference up to your policy limits.

This coverage is particularly relevant when considering budget travel or luxury travel alike; accidents can happen to anyone, and being protected from uninsured or underinsured drivers is a significant safeguard.

Liability Limits and Peace of Mind

Increasing your Bodily Injury Liability (BIL) limits is one of the most crucial steps you can take to protect your financial future. Imagine the cost of a serious accident involving multiple vehicles and severe injuries. Even a $100,000 policy might not be enough. Many financial planners recommend liability limits of $100,000/$300,000 or even higher, especially if you have significant assets to protect.

When planning your Florida travel, whether it’s a family trip to Universal Studios or a leisurely drive along Ocean Drive in Miami Beach, ensuring your auto insurance is up-to-date and adequate is a fundamental part of responsible planning. This peace of mind allows you to fully enjoy the diverse experiences and attractions that Florida has to offer, from the historical charm of St. Augustine to the natural beauty of the Everglades.

How Insurance Affects Accommodation and Lifestyle Choices

Your insurance decisions can indirectly influence your accommodation and lifestyle choices in Florida. For instance, if you plan an extended stay in Florida, perhaps a long-term apartment rental or a villa, having robust car insurance can provide greater confidence when exploring local culture, trying out different restaurants, and engaging in various activities.

If you are a luxury traveler considering a high-end vehicle for your stay at a luxury resort, you will likely opt for more comprehensive insurance to match the value of your chosen transportation and accommodation. Conversely, if you are on a budget travel itinerary, you might be more inclined to ensure you have sufficient liability coverage to avoid any unexpected expenses that could derail your trip.

Ultimately, understanding and adhering to Florida’s car insurance laws is not just a legal obligation; it’s a vital step in safeguarding yourself, your finances, and your ability to fully enjoy your time in the Sunshine State. Whether you’re planning a short visit or a more permanent relocation, make sure your travel insurance and your auto insurance work in harmony to provide complete protection.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.