Navigating the complexities of estate planning and the financial implications that follow can be a daunting task for anyone. For those who own property or have loved ones residing in the Sunshine State, a common question arises: “Is there an inheritance tax in Florida?” Understanding Florida’s tax landscape is crucial for ensuring that your assets are transferred smoothly and efficiently to your beneficiaries. This article will delve into the nuances of inheritance and estate taxes in Florida, exploring what they are, who they affect, and how individuals can plan accordingly. We’ll also touch upon how these financial considerations might intersect with lifestyle choices, travel, and accommodation plans within the state.

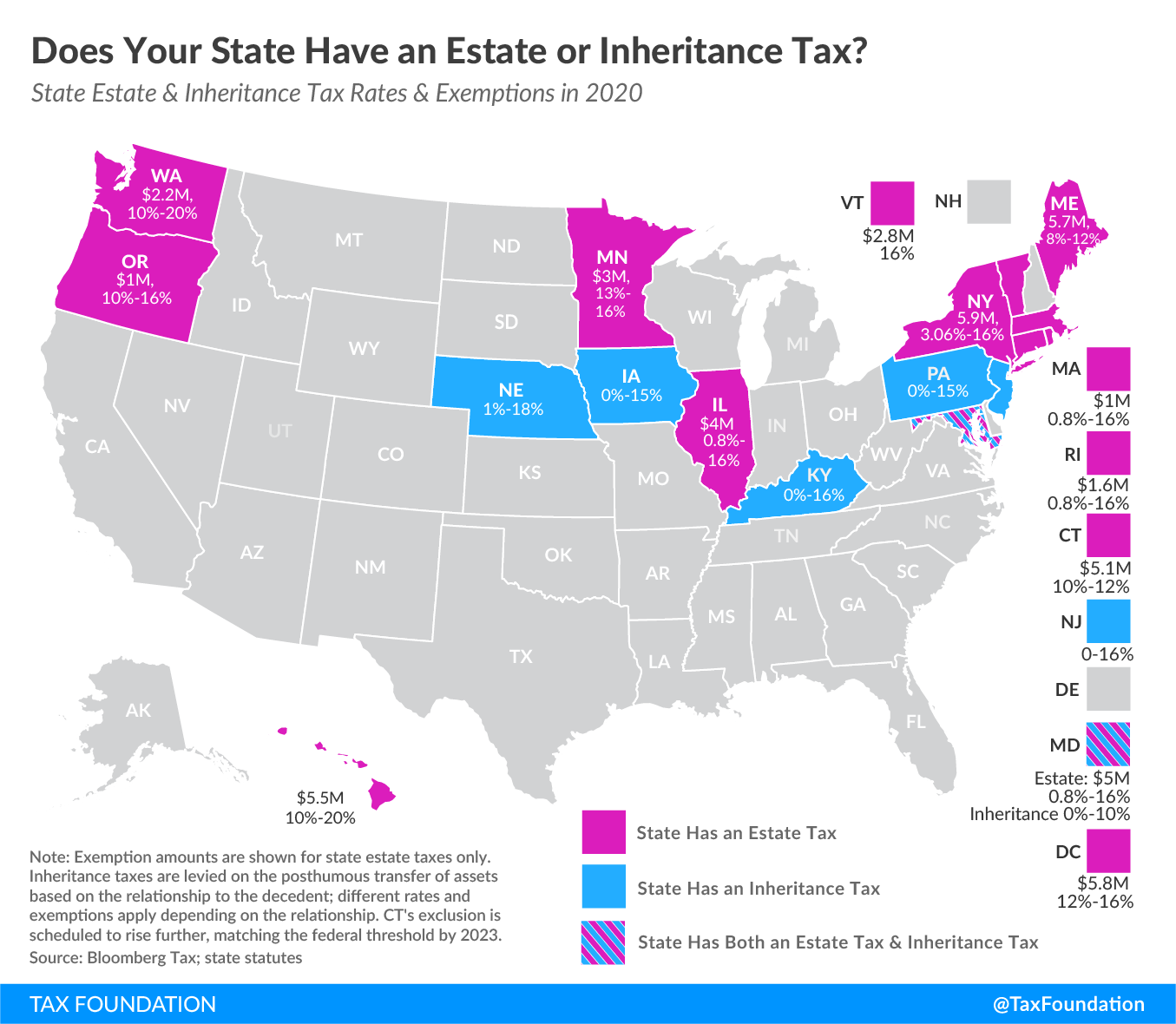

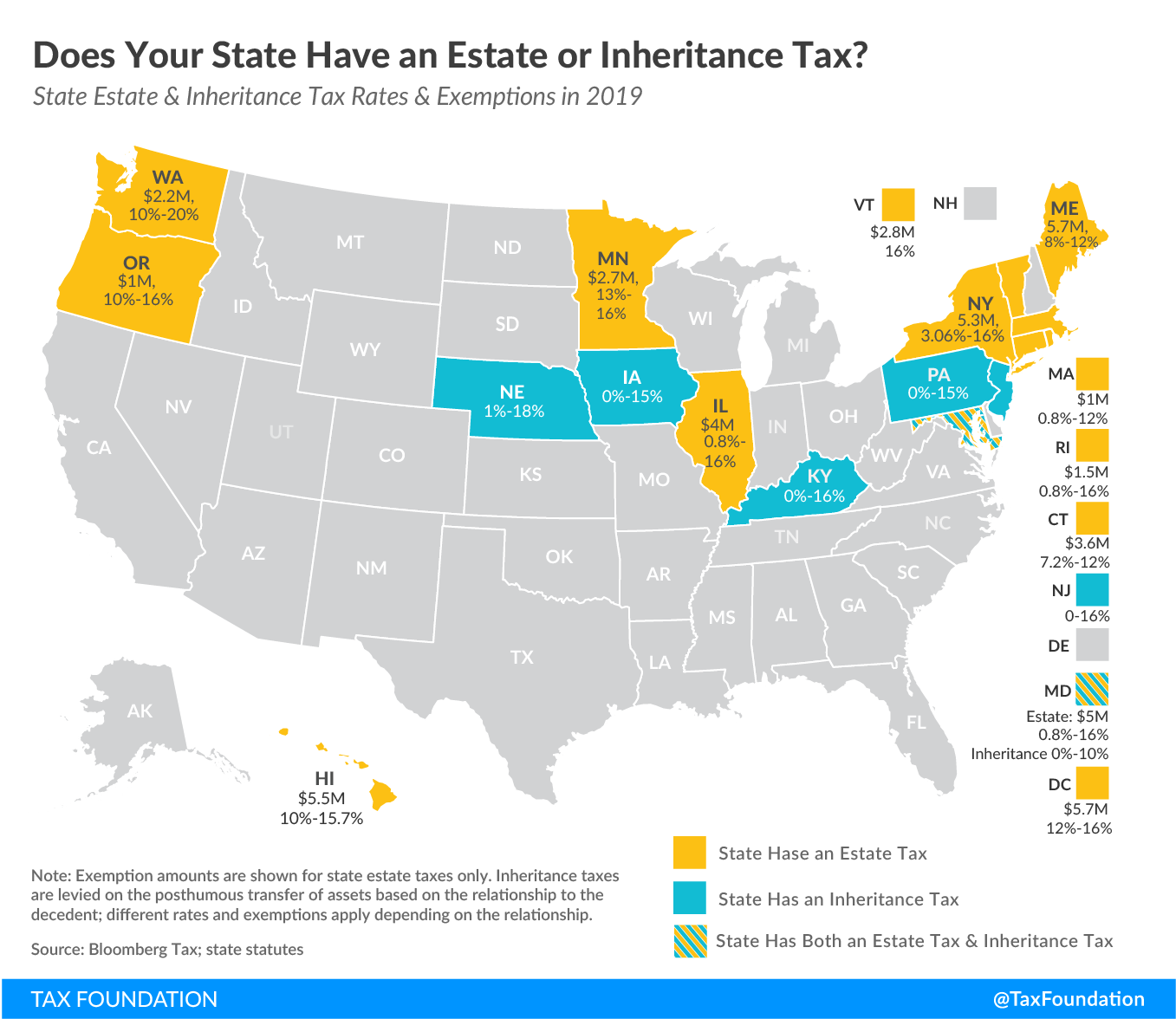

Florida, a popular destination for both permanent residents and tourists seeking sunshine and vibrant experiences, has a distinct approach to taxation. Unlike many other states, Florida has deliberately chosen not to impose an inheritance tax. This can be a significant advantage for those planning their estates or inheriting assets within the state. However, it’s important to understand that the absence of an inheritance tax doesn’t mean there are no tax considerations at all. There are federal estate taxes to consider, and understanding the differences is key.

Understanding Florida’s Tax Landscape: Inheritance vs. Estate Tax

The terms “inheritance tax” and “estate tax” are often used interchangeably, but they refer to distinct types of taxes with different implications for both the deceased and the beneficiaries. Clarifying these definitions is the first step in understanding Florida’s tax environment.

Inheritance Tax Explained

An inheritance tax is levied on the beneficiaries who receive assets from an estate. The tax rate can vary depending on the relationship between the beneficiary and the deceased. For instance, a spouse or child might have a different tax rate than a more distant relative or a friend. This tax is paid by the recipient of the inheritance. Currently, Florida does not have an inheritance tax. This means that if you inherit assets from a Florida resident, you generally won’t have to pay a state-level tax on those assets, regardless of your relationship to the deceased. This can be a significant relief for beneficiaries, especially when inheriting substantial wealth. The absence of an inheritance tax makes Florida an attractive state for individuals to establish residency and plan their estates, knowing that their loved ones will receive a larger portion of their assets without this particular state tax burden. This can influence decisions about where to retire or where to invest in property for vacation homes or long-term stays.

Estate Tax Explained

An estate tax, on the other hand, is a tax levied on the total value of a deceased person’s estate before it is distributed to beneficiaries. This tax is paid by the estate itself. States that impose an estate tax typically set a certain threshold. If the total value of the estate exceeds this threshold, the estate tax is applied to the amount above that exemption limit.

While Florida does not have its own state estate tax, it is subject to the federal estate tax. The Internal Revenue Service (IRS) imposes a federal estate tax on larger estates. The federal estate tax exemption amount is quite high, meaning that only a small percentage of the wealthiest estates are subject to this tax. For 2023, the federal estate tax exemption was $12.92 million per individual, and for 2024, it is $13.61 million per individual. This means that an individual can pass on assets up to this substantial amount without incurring federal estate tax. For couples, this exemption can be effectively doubled through portability.

The interplay between no state inheritance tax and the federal estate tax is a crucial point for estate planning. Individuals with assets below the federal exemption limit have no state or federal estate or inheritance tax liabilities to worry about in Florida. For those with estates exceeding the federal threshold, careful planning is necessary to mitigate the federal estate tax burden.

Planning for Your Legacy in the Sunshine State

Given Florida’s tax-friendly environment regarding inheritance, many individuals choose to retire or establish residency in the state. This lifestyle choice often involves purchasing property, enjoying the diverse attractions, and planning for future generations. Understanding how to structure your assets and estate can maximize the benefit to your heirs.

Estate Planning Strategies

Effective estate planning is paramount to ensuring your assets are distributed according to your wishes and with minimal tax implications. While Florida has no inheritance tax, other strategies can be employed to manage your estate.

- Wills and Trusts: Having a well-drafted will is fundamental. A will clearly outlines how you want your assets distributed, names an executor to manage your estate, and can appoint guardians for minor children. For larger estates or specific circumstances, trusts can offer additional benefits. A revocable living trust, for example, can allow assets to pass to beneficiaries outside of the probate process, which can be faster and more private. Trusts can also be structured for tax efficiency, particularly in relation to the federal estate tax.

- Gifting: The IRS allows individuals to make gifts during their lifetime without incurring gift tax, up to an annual exclusion amount. For 2023, this was $17,000 per recipient, and for 2024, it is $18,000 per recipient. Beyond the annual exclusion, individuals can also use their lifetime gift tax exclusion, which is unified with the estate tax exclusion. Strategically gifting assets during your lifetime can reduce the taxable value of your estate, potentially bringing it below the federal estate tax threshold.

- Life Insurance: Life insurance policies can be structured to provide a tax-free death benefit to your beneficiaries. In some cases, life insurance can be held in an irrevocable life insurance trust (ILIT) to remove the death benefit from your taxable estate altogether. This can be a valuable tool for estate planning, especially for larger estates.

- Real Estate and Investments: Florida is a popular state for real estate investment, whether it’s a luxury villa in Miami, a beachfront resort in Clearwater, or a family home in Orlando. The value of these properties forms a significant part of an individual’s estate. When planning, consider how these assets will be valued and passed on. For non-Florida residents who own property in Florida, understanding the implications of their home state’s tax laws is also crucial.

The Influence of Lifestyle and Travel on Estate Planning

The vibrant lifestyle offered by Florida, from its world-renowned theme parks in Orlando and the stunning beaches of the Florida Keys to the cultural hubs of Tampa and St. Petersburg, often influences people’s decisions about where to live and how to structure their lives. These lifestyle choices can have a direct impact on estate planning.

For instance, individuals who frequently travel or own multiple vacation homes in destinations like Key West or Palm Beach may have a more complex estate to manage. Planning for the distribution of such diverse assets requires careful consideration. The appeal of Florida as a travel destination also means that many people may own property there without being residents. In such cases, the estate may be subject to the laws of multiple states, adding another layer of complexity.

Accommodation choices also play a role. Whether someone opts for a luxurious suite at the Ritz-Carlton Amelia Island, a family-friendly resort like Walt Disney World Resorts, or a long-term apartment rental in Fort Lauderdale, the nature and value of these assets need to be factored into estate planning. Similarly, those who invest in vacation rentals or villas might consider how these income-generating properties will be managed and passed on to heirs.

The tourism sector in Florida is a massive economic driver, and many individuals build their wealth through businesses related to this industry. Planning for the succession of such businesses is a critical component of estate planning, ensuring continuity and preserving value for future generations. Landmarks like Everglades National Park or the historic St. Augustine attract millions of visitors, and owning businesses that cater to these tourists, such as hotels or tour operators, requires robust estate planning to ensure the business’s future.

Navigating Federal Estate Tax and Florida Law

While Florida’s lack of an inheritance tax is a significant benefit, it’s vital to remember the federal estate tax. Even with a high exemption, very large estates can still be subject to this tax. Careful planning is essential for those who anticipate their estates exceeding the federal threshold.

- Portability: For married couples, “portability” allows the surviving spouse to use any unused portion of the deceased spouse’s federal estate tax exemption. This can effectively double the amount that can be passed on tax-free. Electing portability requires filing a federal estate tax return (Form 706) even if the estate is below the taxable threshold.

- Irrevocable Trusts: For individuals with estates likely to exceed the federal exemption, irrevocable trusts can be a powerful tool. These trusts are designed to remove assets from the grantor’s taxable estate. Examples include Irrevocable Life Insurance Trusts (ILITs) and Grantor Retained Annuity Trusts (GRATs).

- Professional Advice: Given the complexities of estate and tax law, especially when dealing with the federal estate tax, seeking advice from qualified professionals is highly recommended. Estate planning attorneys, financial advisors, and certified public accountants (CPAs) can provide tailored guidance based on your specific financial situation and goals. They can help you understand the nuances of Florida law and federal tax regulations, ensuring your estate plan is as efficient and effective as possible.

In conclusion, the answer to “Is there an inheritance tax in Florida?” is a clear no. This makes Florida a very attractive state for estate planning and for those looking to relocate their retirement plans or invest in property. However, the absence of a state inheritance tax does not negate the importance of comprehensive estate planning. Understanding the federal estate tax, utilizing tools like wills and trusts, considering gifting strategies, and seeking professional advice are all crucial steps in ensuring your legacy is preserved and passed on smoothly to your loved ones, allowing them to fully enjoy the beauty and opportunities that Florida has to offer.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.