California, often hailed as the Golden State, beckons millions of travelers, businesses, and new residents each year with its diverse landscapes, iconic landmarks, vibrant culture, and unparalleled lifestyle opportunities. From the sun-drenched beaches of San Diego to the bustling metropolis of Los Angeles, the artistic charm of San Francisco, and the serene vineyards of Napa Valley, there’s an endless array of experiences waiting to be discovered. Whether you’re planning a dream vacation to Disneyland Resort, a business trip to Silicon Valley, or considering a long-term stay, understanding the local regulations is crucial for a smooth and enjoyable experience. One such regulation that often catches visitors and newcomers by surprise is the California Use Tax.

While most people are familiar with sales tax – the amount added to the price of goods and services purchased directly from a retailer – the use tax serves as its lesser-known, yet equally important, counterpart. It’s designed to ensure fairness and prevent a revenue loss for the state when sales tax isn’t collected at the point of purchase. For those involved in the travel industry, from luxury Hotels and Resorts to individual travelers seeking unique experiences and even businesses providing Accommodation services, understanding the intricacies of the California Use Tax is not just a legal obligation but a practical necessity for seamless financial planning and compliance. This comprehensive guide will demystify the California Use Tax, explaining its purpose, who it applies to, common scenarios where it’s incurred, and how to ensure you remain compliant while enjoying all that California has to offer.

Understanding the Fundamentals of California Use Tax

At its core, the California Use Tax is an excise tax levied on the storage, use, or consumption of tangible personal property purchased from an out-of-state vendor for use within California, when the seller does not collect California sales tax. Think of it as a compensatory tax – it makes sure that purchases from outside the state are taxed at the same rate as those made within California, thus preventing an unfair advantage for out-of-state retailers and ensuring that the state’s vital services are adequately funded.

The Rationale Behind the Use Tax

The primary reason for the existence of the use tax is to protect California businesses and maintain a level playing field. Without it, residents and businesses could theoretically bypass California sales tax by purchasing goods from retailers located in other states or countries that do not have nexus (a significant presence) in California and therefore are not required to collect California sales tax. This would not only disadvantage local California businesses, which are legally obliged to collect sales tax, but also significantly diminish the state’s revenue, impacting essential public services that benefit everyone, including tourists and businesses. From road maintenance and public safety to education and environmental protection – the very infrastructure that supports California’s tourism and lifestyle sectors – sales and use tax revenues play a critical role.

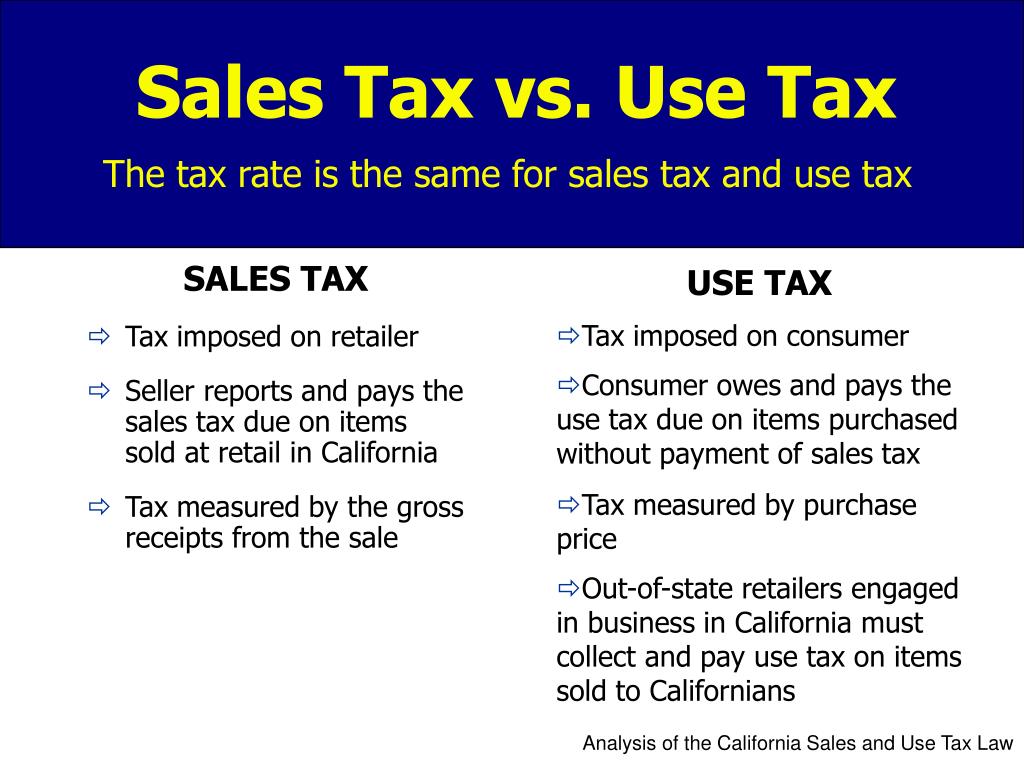

Sales Tax vs. Use Tax: A Key Distinction

While closely related, sales tax and use tax operate under different circumstances.

- Sales Tax: This is a tax on retail sales of tangible personal property within California. It is collected by the seller at the time of purchase and remitted to the state. When you buy a souvenir at a gift shop near Universal Studios Hollywood or a bottle of wine in Napa Valley, you’re paying sales tax.

- Use Tax: This is a tax on the use, consumption, or storage of tangible personal property in California when the seller did not collect California sales tax. The responsibility for reporting and paying use tax generally falls on the purchaser. This distinction is vital, as it means that even if a seller doesn’t charge you sales tax, you might still owe use tax to the state of California. The use tax rate is the same as the sales tax rate in effect at the location where the property is used, stored, or consumed.

Who Needs to Pay: Travelers, Residents, and Businesses

The scope of the California Use Tax is broad, extending its reach to individuals and entities across various categories, all of whom contribute to the vibrant economy and dynamic lifestyle of the state.

For the California Traveler and Tourist

If you’re visiting California for leisure or business, the use tax might seem less relevant, as most of your purchases will likely be made within the state and subject to sales tax. However, consider these scenarios:

- Bringing Items Purchased Out-of-State/Country: Imagine you purchased a high-value camera or a piece of designer luggage in Oregon (which has no sales tax) or even Europe or Asia (where you paid a different local tax), with the intent to use it primarily during your extended stay or eventual relocation to California. If you bring these items into California for use, you could owe California Use Tax on them. This is particularly relevant for those planning longer stays or even moving to the state.

- Online Purchases Shipped to California: While many large online retailers now collect California sales tax due to evolving nexus laws, smaller out-of-state vendors might not. If you order a specialty item for your trip, say, unique camping gear for a journey to Lake Tahoe or a specific outfit for an event in Beverly Hills, and the out-of-state seller doesn’t charge sales tax, you’re responsible for declaring and paying the use tax.

Implications for California Residents and Those Relocating

For permanent or long-term residents, and especially those moving to California, the use tax is a more frequent consideration.

- Online Shopping: This is perhaps the most common scenario. If you regularly shop online from retailers located outside California that don’t collect sales tax (e.g., small businesses, specialized vendors), you are accruing a use tax liability. This applies to everything from books and electronics to furniture and clothing.

- Purchases Made During Out-of-State Travel: If you take a road trip to Nevada or Arizona and buy significant items like art, electronics, or even a vehicle from a seller who doesn’t collect California sales tax, you’ll owe use tax when you bring those items back for use in California.

- Relocation: Individuals moving to California from another state or country (such as Mexico or Canada) might bring personal property, including household goods, furniture, and vehicles, that were purchased outside California. If these items were acquired less than 90 days before moving into California and were not used outside the state prior to entry, they may be subject to use tax. There are specific rules and exemptions for household goods acquired more than 90 days prior to relocation, which can be complex.

Business Operations and Use Tax

Businesses, from small boutique shops in Carmel-by-the-Sea to sprawling Resorts in Palm Springs and professional services firms in Sacramento, frequently deal with use tax.

- Purchases of Equipment and Supplies: A new hotel opening in Los Angeles might purchase custom furniture from a manufacturer in North Carolina or specialized kitchen equipment from a supplier in Illinois. If these out-of-state vendors do not have a physical presence in California and therefore do not charge California sales tax, the hotel is responsible for reporting and paying the use tax on those purchases. This also applies to office supplies, computer equipment, marketing materials, and any other tangible personal property used in the course of business.

- Services with Tangible Personal Property: Sometimes, a service contract includes the provision of tangible personal property. For example, a marketing agency might hire an out-of-state printer for brochures to be distributed in California. If the printer does not charge sales tax, the marketing agency might owe use tax on the printed materials.

- Goods for Resale vs. Own Use: Businesses generally don’t pay sales or use tax on items they purchase for resale. However, if a business purchases items that they intend to use internally (e.g., display cases, cleaning supplies, new linens for a hotel) and sales tax was not collected, use tax applies.

Common Scenarios Where Use Tax Applies in the Golden State

To better illustrate the practical implications, let’s explore some common scenarios relevant to the travel, accommodation, and lifestyle themes.

Online Purchases and Out-of-State Retailers

This is by far the most prevalent situation for both individuals and businesses. The rise of e-commerce has made it incredibly easy to purchase goods from anywhere in the world.

- Example for an Individual: A resident in San Francisco orders a unique handcrafted vase from an artisan’s website based in New York. The artisan, a small business, does not have any physical presence in California and thus does not charge sales tax. When the vase is delivered and brought into California for use, the San Francisco resident is responsible for paying the use tax.

- Example for a Business: A boutique hotel in Napa Valley orders custom robes and slippers from a specialized manufacturer in Georgia for their guest rooms. If the manufacturer, lacking nexus in California, does not collect sales tax, the Napa Valley hotel must self-assess and pay the use tax on these items.

Bringing Goods into California

This scenario is particularly pertinent to travelers and those relocating.

- Example for a Traveler/New Resident: A family moving from Texas to Los Angeles purchased a new, high-end home theater system just a month before their move. Since it was purchased outside California and used for a short period before being brought into the state, it would likely be subject to California Use Tax. If they had purchased the system a year ago and used it extensively in Texas, it would likely qualify as household goods exempt from use tax upon relocation.

- Example for a Business Trip: An executive on a business trip to Japan buys a new, specialized laptop for their work back in Silicon Valley. When returning to California and using the laptop for business purposes, the individual or their company would need to report and pay use tax if no sales tax equivalent was collected or if the Japan tax was not equivalent to California sales tax.

Purchases for Hotels, Resorts, and Accommodation Providers

The vast and diverse needs of the hospitality sector mean frequent purchases from various vendors.

- Example: Furniture and Fixtures: A newly renovated hotel like The Pacific Grand Hotel in San Diego sources its lobby furniture and custom artwork from a designer in Florida. If the Florida designer does not have a nexus in California and doesn’t collect sales tax, The Pacific Grand Hotel must account for and remit the use tax to the California Department of Tax and Fee Administration (CDTFA).

- Example: Specialty Supplies: A luxury resort in Palm Springs, Coastal Breeze Resort, orders custom-branded toiletries from an exclusive supplier in France or Italy. These supplies, intended for use by guests within the resort, would be subject to use tax upon their arrival and use in California.

Navigating California Use Tax for a Seamless Experience

Compliance with California’s tax laws, including the use tax, is crucial for both individuals and businesses. Ignoring these obligations can lead to penalties, interest, and unwelcome audits, potentially tarnishing an otherwise delightful California experience or business venture.

How to Report and Pay Use Tax

The method for reporting and paying use tax varies depending on whether you are an individual or a business.

- For Individuals: Most individuals report and pay use tax annually through their California income tax return (Form 540). There’s usually a line item where you can declare your total use tax liability for the year. Alternatively, if your purchases exceed a certain threshold or you prefer to pay separately, you can do so directly through the California Department of Tax and Fee Administration (CDTFA) website.

- For Businesses: Businesses that hold a seller’s permit in California typically report and pay use tax on their regular sales and use tax returns. Businesses that do not hold a seller’s permit but have a use tax liability can register with the CDTFA and file a Consumer Use Tax Return. Maintaining meticulous records of all out-of-state purchases is vital for accurate reporting.

Key Exemptions to Consider

While the use tax applies broadly, there are several exemptions that could relieve you of the obligation in specific circumstances. Some common exemptions include:

- Property Used Out-of-State: If you purchased an item outside California and used it substantially in another state or country before bringing it into [California](https://lifeoutofthebox.com/california], it might be exempt. The definition of “substantially” often involves a minimum period of use (e.g., 90 days). This is particularly relevant for those relocating to California.

- Property Subject to Sales Tax: If the seller already collected and remitted California sales tax (or a sales tax from another state/country that is credited against California’s use tax), you do not owe use tax. You generally receive a credit for sales tax paid in another state or a foreign country against the California use tax. However, if the out-of-state tax was lower, you might still owe the difference.

- Property Purchased for Resale: As mentioned, businesses are generally not taxed on items they purchase with the sole intent of reselling them.

- Specific Exemptions: Certain types of property or transactions may be specifically exempted by law, such as food products for home consumption, prescription medicines, or specific agricultural equipment. It’s always best to consult the CDTFA or a tax professional for the most accurate and up-to-date information regarding specific exemptions.

The Importance of Compliance for Peace of Mind

Navigating the tax landscape, even in a beautiful place like California, can seem daunting. However, understanding and complying with the use tax ensures that you contribute to the state’s welfare while avoiding potential legal and financial repercussions. For travelers, it means a hassle-free trip focused on enjoying world-class destinations; for residents, it’s about responsible citizenship; and for businesses, it underscores operational integrity and avoids costly penalties. The California Department of Tax and Fee Administration (CDTFA) provides extensive resources, including publications, online guides, and customer service, to assist taxpayers in understanding their obligations. When in doubt, especially for complex business transactions or significant personal purchases, consulting with a tax professional experienced in California tax law is always a wise decision.

In conclusion, the California Use Tax is a fundamental component of the state’s revenue system, designed to complement sales tax and ensure equitable taxation on goods consumed within its borders. Whether you’re visiting California for its famous landmarks, indulging in its unique lifestyle, staying in its luxurious hotels, or running a business that benefits from its thriving economy, being aware of and complying with the use tax is essential for a smooth and enjoyable experience in the Golden State.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.