Navigating the intricacies of taxation can often feel like deciphering an ancient map, especially when dealing with a jurisdiction as dynamic as California. For many, the question “What tax bracket am I in California?” is not just about financial planning; it’s about understanding how their income translates into disposable income for life’s adventures, from a lavish resort stay in Napa Valley to a budget-friendly exploration of Joshua Tree National Park. This article aims to demystify California’s income tax system, providing a clear pathway to understanding your tax bracket and its implications for your lifestyle choices, whether you’re planning a dream vacation or managing your everyday finances.

California, a state renowned for its stunning coastlines, vibrant cities like Los Angeles and San Francisco, and diverse attractions, also boasts a progressive income tax structure. This means that as your income increases, so does the percentage of that income you contribute to the state. Understanding your position within this structure is crucial for financial management, enabling informed decisions about everything from travel budgets to investment strategies. We’ll break down the key components of California’s tax brackets, how they are determined, and what this means for your personal finance and leisure pursuits.

Understanding California’s Progressive Income Tax System

At its core, California’s income tax system is designed to ensure that those with higher earning capacities contribute a larger proportion of their income towards public services and infrastructure. This progressive approach is common across many states and at the federal level, aiming for a more equitable distribution of the tax burden. For residents of California, understanding this system is the first step in accurately determining their tax bracket.

How Income Tax Brackets Work

Tax brackets are ranges of income that are taxed at specific rates. In a progressive system, as your taxable income rises, it moves into higher tax brackets, and the portion of your income falling into those higher brackets is taxed at a higher rate. It’s a common misconception that if you move into a higher tax bracket, your entire income is taxed at that higher rate. This is not the case. Instead, your income is taxed in segments. For instance, the first portion of your income is taxed at the lowest rate, the next portion at a slightly higher rate, and so on, until your total taxable income has been accounted for.

For example, if the first bracket is 2% for income up to $10,000, and the second bracket is 4% for income between $10,001 and $30,000, an individual earning $20,000 would pay 2% on the first $10,000 and 4% on the $10,000 that falls into the second bracket. Their total tax would be the sum of these two amounts, not 4% on the entire $20,000. This tiered system is fundamental to understanding your overall tax liability.

Key Factors Determining Your Tax Bracket

Several factors influence which tax bracket you fall into in California. The most significant is your Adjusted Gross Income (AGI). AGI is your gross income minus certain “above-the-line” deductions, such as contributions to a traditional IRA, student loan interest payments, and self-employment tax deductions. This figure represents the income upon which your tax liability is primarily calculated.

Beyond AGI, your filing status plays a crucial role. Whether you file as Single, Married Filing Separately, Married Filing Jointly, Head of Household, or Qualifying Widow(er) significantly impacts the income thresholds for each tax bracket. The state of California provides different bracket structures for each filing status to account for varying household financial situations. For instance, married couples filing jointly often have higher income thresholds for tax brackets compared to single filers, reflecting the combined income of two individuals.

Furthermore, understanding taxable income is vital. This is not the same as your AGI. Taxable income is calculated by taking your AGI and subtracting your deductions. You can choose between the standard deduction or itemized deductions. Itemized deductions can include expenses like state and local taxes (up to a certain limit), mortgage interest, charitable contributions, and medical expenses exceeding a certain percentage of your AGI. The choice between these deductions can directly affect your taxable income, and consequently, your tax bracket.

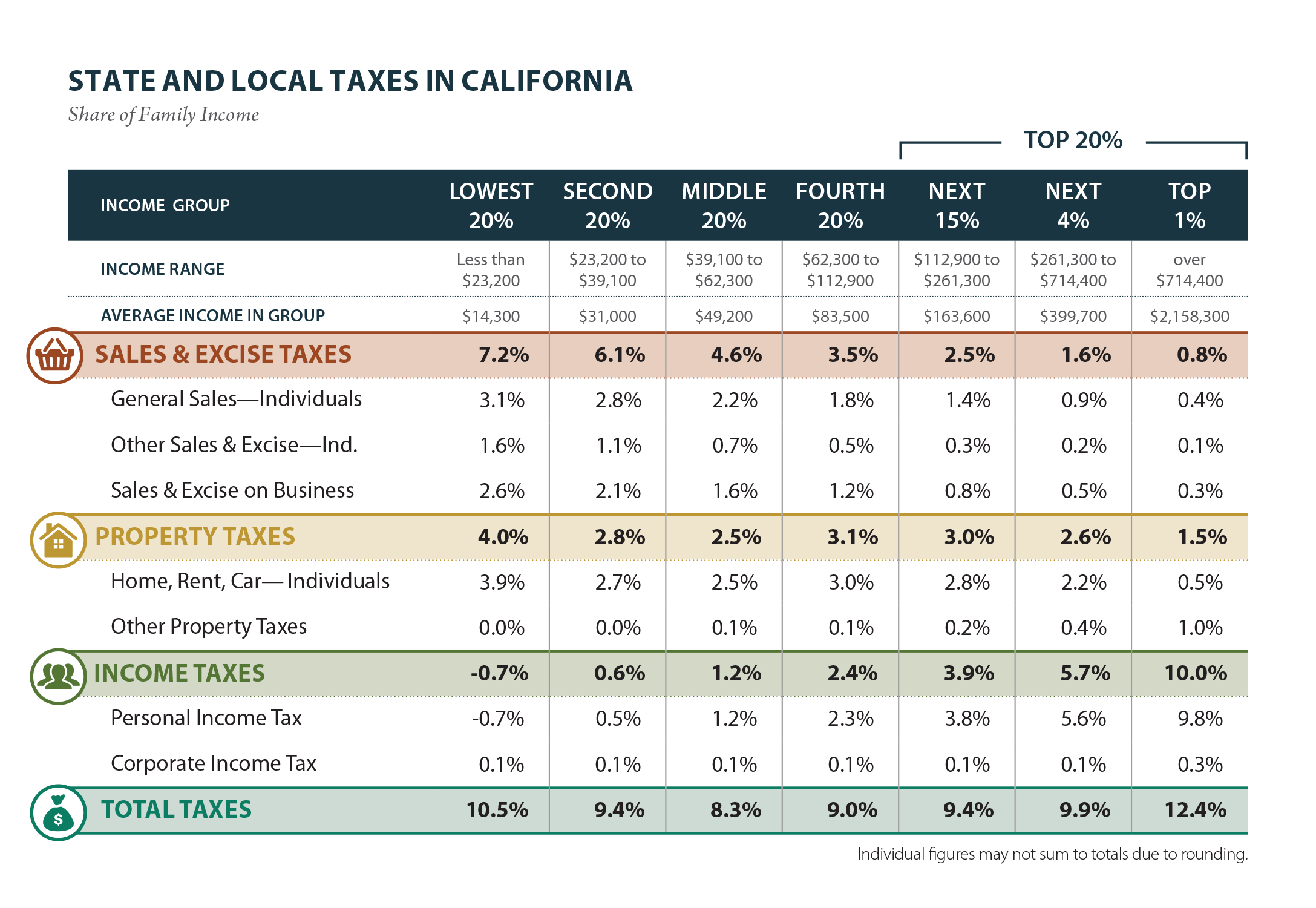

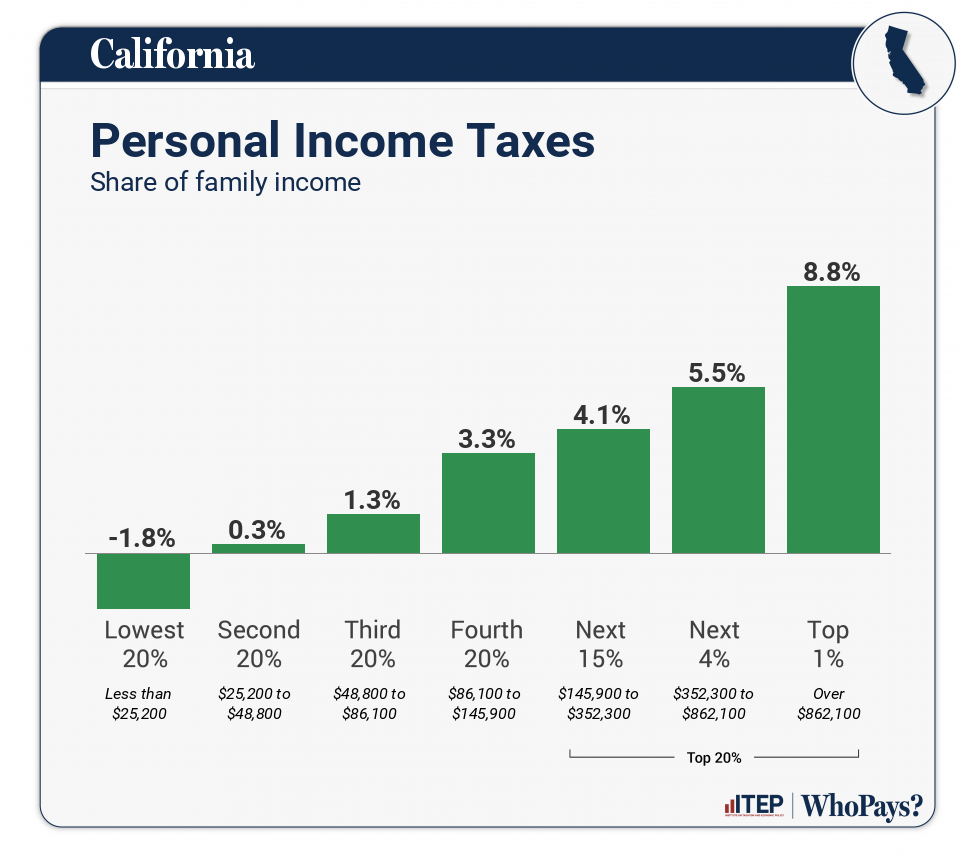

California’s Income Tax Brackets for the Current Tax Year

To accurately answer “What tax bracket am I in California?”, you need to consult the official tax bracket schedules released annually by the California Franchise Tax Board (FTB). These brackets are adjusted for inflation each year, meaning the income ranges for each bracket can shift slightly.

It’s important to note that there are typically multiple sets of tax brackets, differentiated by filing status. For the purpose of this discussion, we’ll outline the general structure and provide illustrative examples.

Tax Brackets by Filing Status

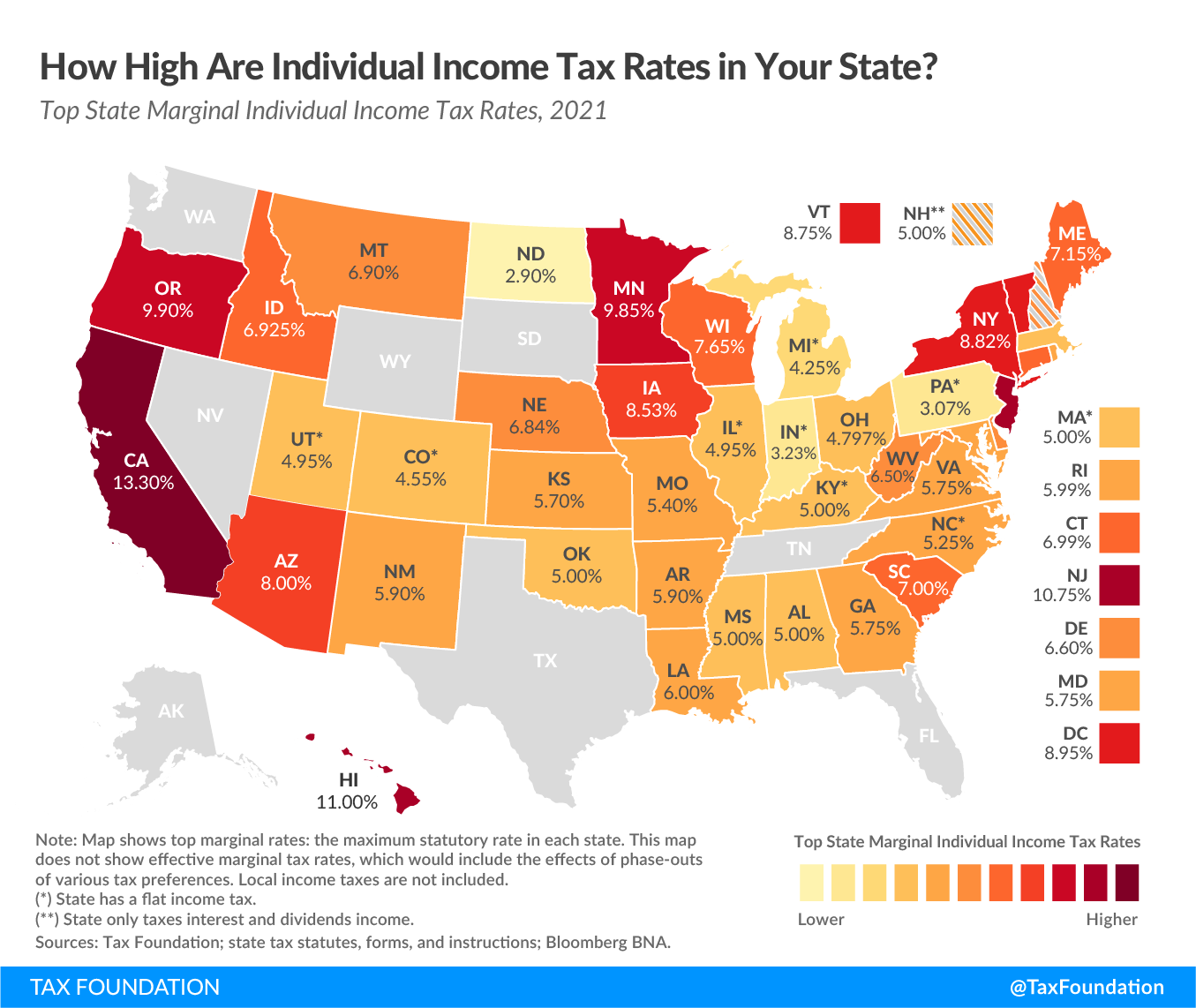

Single Filers: For individuals who are not married and do not qualify for Head of Household status, the tax brackets are set according to their individual income. As of the most recent available tax year information, California has several tax brackets. For example, a single filer might see rates ranging from 1% on the lowest income portion up to 13.3% on the highest portion of their taxable income. The exact income thresholds for each percentage are published by the FTB.

Married Filing Jointly: Couples who file their taxes together benefit from a consolidated income assessment. The income thresholds for each tax bracket are generally doubled compared to single filers. This reflects the combined earnings of both spouses, allowing them to earn more before moving into higher tax brackets. This can be a significant tax advantage for married couples, especially if both partners have substantial incomes.

Married Filing Separately: Individuals who are married but choose to file separate tax returns will have their income taxed according to the single filer brackets. Each spouse is responsible for reporting their own income and claiming their own deductions. This option is sometimes chosen for strategic reasons related to deductions or tax credits, but it typically results in a higher overall tax liability compared to filing jointly.

Head of Household: This status is available to unmarried individuals who pay more than half the cost of keeping up a home for a qualifying child or other eligible dependent. The tax brackets for Head of Household filers fall between those for single filers and married couples filing jointly, recognizing the financial responsibilities associated with supporting a household.

Practical Steps to Determine Your Bracket

- Gather Your Income Information: Compile all sources of income, including wages, salaries, tips, bonuses, self-employment income, interest, dividends, capital gains, and any other earnings.

- Calculate Your Adjusted Gross Income (AGI): Subtract eligible “above-the-line” deductions from your gross income.

- Determine Your Deductions: Decide whether to take the standard deduction or itemize your deductions. If itemizing, list all eligible expenses.

- Calculate Your Taxable Income: Subtract your chosen deductions (standard or itemized) from your AGI.

- Identify Your Filing Status: Determine if you will file as Single, Married Filing Jointly, Married Filing Separately, Head of Household, or Qualifying Widow(er).

- Consult the Official Tax Brackets: Refer to the most current tax rate schedules provided by the California Franchise Tax Board (FTB) for your specific filing status. Locate the income range that your taxable income falls within.

For example, if you are a single filer with a taxable income of $60,000, you would consult the single filer tax bracket table for the current year. You would see that a portion of your income is taxed at, say, 6%, another portion at 8%, and so on, until the full $60,000 is accounted for. The highest rate applied to any portion of your income determines the top tax bracket you are in.

Implications of Your Tax Bracket for Lifestyle and Travel

Understanding your California tax bracket is more than just an annual obligation; it has tangible effects on your financial well-being and, consequently, your lifestyle choices, especially concerning travel and leisure.

Budgeting for Travel and Experiences

Your tax bracket directly influences the amount of discretionary income you have available. If you find yourself in a higher tax bracket, a larger portion of your earnings will be allocated to taxes, leaving less for other expenditures. This means that when planning a vacation, whether it’s a luxurious escape to a boutique hotel in Santa Barbara or a family road trip to see the Golden Gate Bridge, you’ll need to adjust your budget accordingly.

Individuals in higher brackets might need to consider more budget-friendly options, such as exploring state parks instead of international destinations, opting for vacation apartments over high-end resorts, or timing their trips during the off-season to take advantage of lower accommodation prices. Conversely, those in lower tax brackets may find they have more flexibility to indulge in premium travel experiences, perhaps a stay at the iconic Beverly Hills Hotel or a gourmet food tour through Sonoma.

Impact on Investment and Savings Goals

Your tax bracket also affects your long-term financial planning, including savings and investment strategies, which indirectly impact your ability to fund future travel or lifestyle upgrades. High earners in top tax brackets may benefit more from tax-advantaged investment vehicles like 401(k)s and IRAs, as deductions for these contributions reduce their taxable income at a higher rate.

Understanding these implications can help you make informed decisions about where to invest your money and how much to save. This financial foresight can empower you to achieve your lifestyle goals, whether that’s early retirement for extended travel, purchasing a vacation home, or simply having the peace of mind to enjoy life’s experiences without financial strain. For instance, optimizing your tax strategy could free up funds that could be used for a memorable family trip to Disneyland or a solo adventure exploring the natural beauty of Yosemite National Park.

Maximizing Deductions and Credits

Regardless of your tax bracket, a thorough understanding of available deductions and credits can help reduce your tax liability. This could mean more money available for your next holiday or simply a stronger financial footing. Exploring options for deductions related to business expenses, education, or even certain charitable contributions can make a difference. Tax credits, which directly reduce your tax bill dollar-for-dollar, are particularly valuable. Staying informed about potential credits for energy efficiency, child care, or educational expenses can lead to significant savings.

Ultimately, the question “What tax bracket am I in California?” is a gateway to understanding your financial landscape. By arming yourself with this knowledge, you can make smarter financial decisions, plan your travel more effectively, and ultimately, live a richer, more fulfilling lifestyle. Whether your dreams involve exploring the historic missions of San Juan Capistrano, relaxing on the beaches of Malibu, or enjoying the vibrant nightlife of San Diego, a clear grasp of your tax obligations is the first step in making those aspirations a reality.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.