Florida, a sun-drenched paradise, beckons millions of visitors each year with its pristine beaches, vibrant cities like Miami, Orlando, and Tampa, and an enviable lifestyle. From the enchanting theme parks to the serene natural landscapes, the Sunshine State offers an unparalleled experience for travelers, families, and those seeking a permanent or seasonal retreat. As a top destination for travel, tourism, and accommodation, Florida attracts not just vacationers but also a significant number of individuals looking to invest in real estate, whether for a dream vacation home, a long-term residence, or a lucrative rental property. However, owning a slice of this paradise comes with responsibilities, one of the most critical being the timely payment of real estate taxes. Understanding the payment schedule, potential discounts, and penalties is paramount for any property owner or prospective investor in Florida. It’s not just about managing finances; it’s about safeguarding your investment and ensuring continued enjoyment of all that Florida has to offer.

Navigating the intricacies of property taxes can seem daunting, especially for those new to the state or international investors. But with a clear understanding of the system, it becomes a straightforward process. This comprehensive guide aims to demystify when Florida real estate taxes are due, shedding light on the annual cycle, opportunities for savings, and the consequences of oversight. Whether you’re a long-time resident, a snowbird enjoying the winter months, or someone dreaming of a future in Florida, knowing these dates and details is a crucial part of smart property management and a stress-free lifestyle in this beautiful state.

The Annual Cycle of Florida Real Estate Taxes: Key Dates and Deadlines

The Florida property tax system operates on a precise annual calendar, with several key dates that property owners must be aware of. Unlike some other states, Florida generally adheres to a consistent schedule for assessment, billing, and collection, making it easier for owners to plan their finances. Understanding this cycle is the first step toward responsible property ownership and avoiding any unexpected surprises.

Key Dates for Property Tax Assessments and Payments

The journey of your annual property tax bill begins long before it ever lands in your mailbox. It starts at the beginning of the calendar year with the assessment phase, which sets the value of your property for tax purposes.

January 1st: The Assessment Day

Every year, on January 1st, all real estate properties in Florida are assessed for tax purposes. This date serves as the official lien date, meaning the property taxes for the upcoming year become a lien on the property as of this day. The value determined by the County Property Appraiser on January 1st dictates the taxable value for the entire year. This assessment takes into account various factors, including market conditions, recent sales of comparable properties, and any improvements made to your property. For those considering buying or selling, it’s crucial to understand that the property’s tax liability for the entire year is tied to its status on this date.

November 1st: Tax Bills Are Mailed

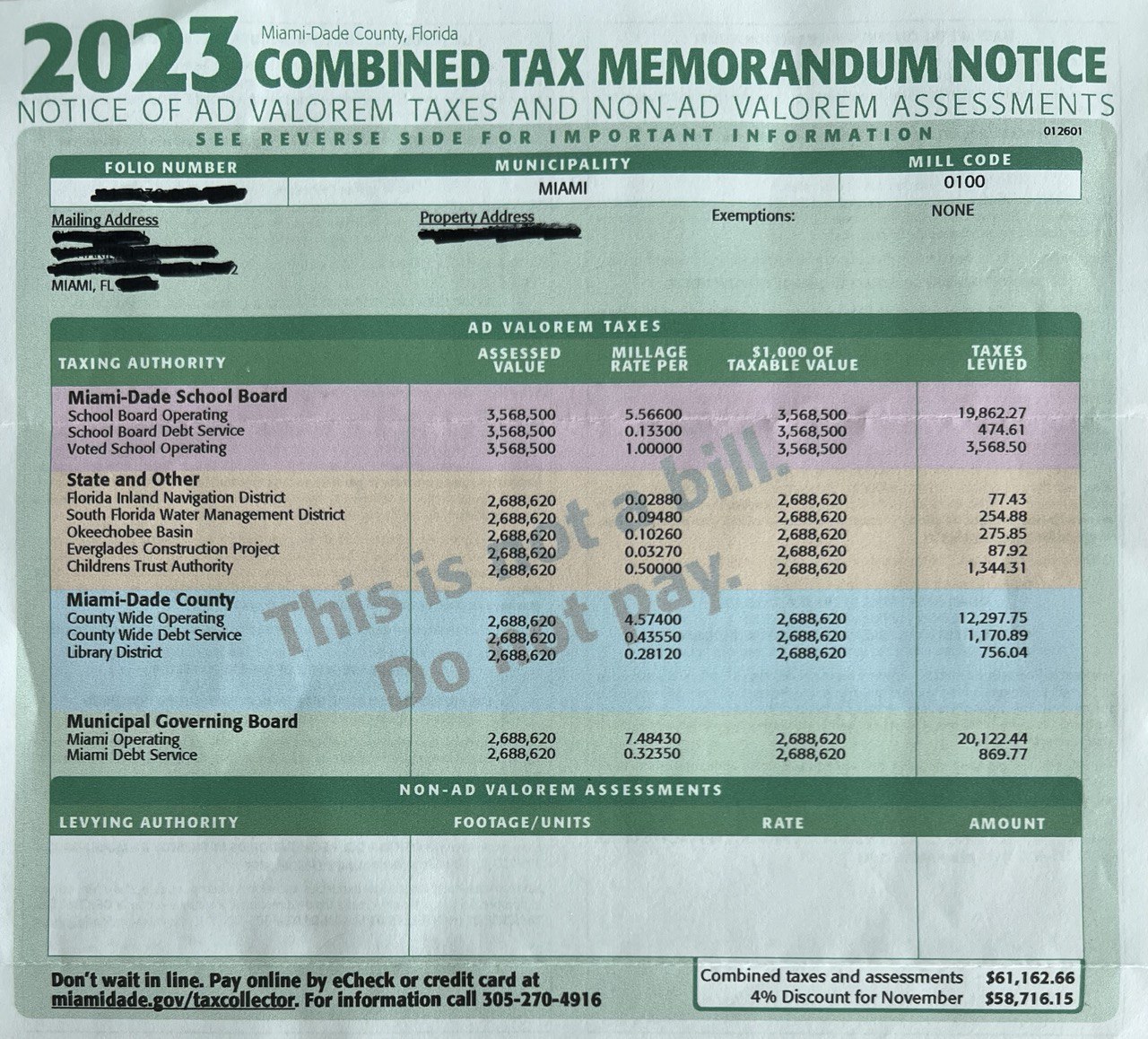

The official tax bills are typically mailed out by the County Tax Collector around November 1st each year. This marks the beginning of the tax collection period, which spans several months. Upon receiving your tax bill, it’s advisable to review it carefully. The bill will detail your property’s assessed value, the taxable value (after any exemptions), the millage rate applied by various taxing authorities (such as the county, city, school board, and water management districts), and the total amount due. This is your cue to begin planning for payment, especially if you intend to take advantage of the early payment discounts. For snowbirds or those who own vacation homes and are not always in Florida during November, it’s important to ensure your mailing address is up-to-date with the Tax Collector’s office or to arrange for electronic delivery of your tax bill. This proactive approach prevents any delays in receiving vital information.

March 31st: The Final Deadline Without Penalty

The standard deadline for paying your Florida real estate taxes without incurring penalties is March 31st of the following year. For example, taxes assessed on January 1st, 2024, and billed on November 1st, 2024, would be due by March 31st, 2025. This gives property owners a five-month window from the billing date to settle their tax obligations. It’s a generous timeframe that also incorporates incentives for early payment, which we’ll delve into shortly. Missing this deadline can lead to significant financial repercussions, as penalties and interest begin to accrue immediately.

April 1st: Delinquency and Penalties Begin

If property taxes remain unpaid after March 31st, they become delinquent on April 1st. This is a critical date, as it triggers the immediate application of penalties and interest, significantly increasing the total amount due. Delinquent taxes are subject to a statutory interest rate and additional fees, and the property can be subject to further enforcement actions, including the sale of tax lien certificates. Understanding the gravity of this date is crucial for all property owners, as timely payment protects your investment from escalating costs and potential legal issues.

Understanding Your Tax Bill and Assessment

Before you even think about payment, it’s essential to understand how your tax bill is calculated and what factors influence it. Each year, your County Property Appraiser is responsible for determining the “just value” of your property, which is essentially its market value. This value is then used to calculate your “assessed value,” and after applying any exemptions, your “taxable value.” The total tax due is then calculated by multiplying your taxable value by the combined millage rates of all the taxing authorities in your area. This includes county government, city services, school districts, water management, and potentially other special districts. The County Tax Collector is then responsible for sending out the bills and collecting the payments. For many property owners, especially those who use their Florida property as a vacation home or part-time residence, comprehending these components is vital for effective budgeting and financial planning.

Discounts and Incentives for Early Payment

Florida offers a unique system of discounts designed to encourage property owners to pay their real estate taxes early. This incentive structure is a win-win: it provides property owners with an opportunity to save money, and it helps the state and local governments collect revenue more efficiently. These discounts can add up, particularly for properties with higher tax liabilities, making early payment a financially savvy decision.

Maximizing Your Savings: The Early Bird Discount Structure

The discount program is tiered, meaning the earlier you pay your taxes after the bills are mailed in November, the greater your savings will be. This structure provides a clear financial incentive to prioritize your property tax payment.

-

4% Discount: If you pay your real estate taxes in November, you are eligible for a substantial 4% discount on the total amount due. For example, on a $5,000 tax bill, this translates to a $200 saving, reducing your payment to $4,800. This is the largest discount available and represents a significant incentive for prompt payment. Many property owners, especially those with substantial tax burdens, plan their finances specifically to take advantage of this four-percent reduction. For those managing multiple properties or high-value real estate as part of their lifestyle or investment portfolio, this saving can be quite considerable.

-

3% Discount: If you pay your real estate taxes in December, the discount drops slightly but is still a generous 3%. Using the same $5,000 example, a 3% discount would save you $150, bringing your payment down to $4,850. While not as high as the November discount, it still offers a meaningful reduction and is a strong motivator for payment within the first two months of the collection period.

-

2% Discount: Paying your taxes in January will earn you a 2% discount. On a $5,000 bill, this is a $100 saving, making the payment $4,900. Even at this stage, the discount provides a tangible benefit, encouraging payment well before the final deadline. For many, January marks the start of a new financial year, and incorporating property tax payment into early-year budgeting makes practical sense.

-

1% Discount: If you wait until February to pay your taxes, you can still receive a 1% discount. For our $5,000 example, this means a $50 saving, with the payment amounting to $4,950. While the smallest of the tiered discounts, it’s still a saving that shouldn’t be overlooked. Every dollar saved contributes to a better lifestyle or investment return in Florida.

-

March: If you pay your taxes in March, no discount is applied, and you pay the full amount due. While there’s no discount, paying in March still ensures you avoid any penalties or interest, as long as it’s paid by the March 31st deadline.

The availability of these discounts provides a strong incentive for property owners to proactively manage their tax obligations. It’s a simple yet effective way to trim expenses, freeing up funds for other lifestyle expenditures, travel experiences, or property enhancements. For anyone with property in Florida, budgeting for early payment is a smart financial strategy.

Navigating Penalties and Delinquency

While Florida offers enticing discounts for early payment, it also implements strict measures for delinquent taxes. Understanding these penalties is as crucial as knowing the discount structure, as failure to pay on time can lead to escalating costs and, in severe cases, the loss of your property. For those who enjoy the Florida lifestyle or invest in its booming tourism industry, protecting their assets means adhering to the tax deadlines.

Consequences of Late Payments and Tax Lien Certificates

As previously mentioned, if your property taxes are not paid by March 31st of the year following the assessment, they become delinquent on April 1st. This is when the financial repercussions begin to take effect.

Interest and Penalties: Once taxes are delinquent, interest charges immediately begin to accrue. The statutory interest rate for delinquent property taxes in Florida is typically 18% per year, calculated monthly from the date of delinquency. This high rate means that even a short delay in payment can significantly increase your total tax liability. In addition to interest, various collection fees and administrative costs are added to the delinquent amount, further compounding the financial burden. These fees cover the administrative efforts of the Tax Collector’s office in pursuing unpaid taxes.

Tax Lien Certificates: The most significant consequence of delinquent taxes in Florida is the sale of tax lien certificates. On or before June 1st (which would be June 1st following the April 1st delinquency), the County Tax Collector is mandated by Florida Statutes to hold a tax certificate sale. In this sale, investors bid on the delinquent tax liens, effectively paying the outstanding taxes on behalf of the property owner. In return, the investor receives a tax lien certificate, which is a legal document representing a lien against the property. This certificate accrues interest at the rate bid by the investor, up to a maximum of 18% per year.

For the property owner, this means that instead of owing the county, they now owe an investor. To clear the lien and prevent further action, the property owner must pay the original delinquent taxes plus all accrued interest and fees to the Tax Collector, who then remits the funds to the tax certificate holder. The existence of a tax lien certificate on a property creates a cloud on the title, making it difficult to sell or refinance until the lien is satisfied. This can be particularly problematic for vacation rental owners or those looking to sell their Florida property as part of their lifestyle changes.

The Tax Deed Sale: What Happens Next?

If the tax lien certificate remains unpaid for a specified period (typically two years after the April 1st delinquency date), the holder of the tax certificate can apply to the Clerk of the Court for a tax deed. This initiates a process that can ultimately lead to the loss of the property.

Application for Tax Deed: Once a tax certificate holder applies for a tax deed, the property is scheduled for a tax deed sale. This is a public auction where the property itself is sold to the highest bidder to satisfy the outstanding taxes, interest, and fees. Before the sale, the Clerk of the Court provides notice to the property owner, any lienholders, and other interested parties. There is a redemption period during which the property owner can still pay the outstanding amount to stop the sale. However, the cost to redeem increases significantly due to additional fees and advertising costs associated with the tax deed application process.

Public Auction and Loss of Property: If the property is not redeemed by the owner before the scheduled tax deed sale, it will be auctioned off to the highest bidder. The proceeds from the sale are used to pay off the tax lien certificate holder, the county, and other eligible lienholders. Any remaining surplus funds, if any, are held for the former property owner. However, if the sale price is less than the total outstanding taxes and costs, the former owner will not receive anything. A tax deed sale is a final and irreversible action, resulting in the complete loss of ownership for the original property owner. This underscores the critical importance of staying informed and current on Florida real estate tax obligations. Losing a valuable Florida property, whether it’s a family vacation spot or a key investment, can have devastating financial and personal consequences.

Essential Property Tax Exemptions and Relief Programs

While property taxes are an unavoidable part of homeownership in Florida, the state offers various exemptions and relief programs that can significantly reduce a property owner’s tax liability. These programs are designed to provide financial relief to permanent residents and specific groups of individuals, making homeownership more affordable and supporting the diverse lifestyles within the Sunshine State. Understanding and applying for these exemptions can lead to substantial savings, allowing property owners to allocate more funds towards enjoying the vibrant Florida lifestyle or managing their investments more effectively.

The Homestead Exemption: A Cornerstone for Florida Residents

The most widely known and utilized property tax exemption in Florida is the Homestead Exemption. This exemption is designed to provide significant tax relief to individuals who permanently reside in their Florida home.

Eligibility and Benefits: To qualify for the Homestead Exemption, the property owner must claim the property as their primary residence as of January 1st of the tax year for which they are applying. This means the owner must reside in the home, register to vote in Florida (if eligible), have a Florida driver’s license, and generally establish Florida as their legal domicile.

The Homestead Exemption can reduce the assessed value of a primary residence by up to $50,000. Specifically, the first $25,000 of the assessed value is exempt from all property taxes, including school district taxes. An additional $25,000 exemption applies to the assessed value between $50,000 and $75,000, but this portion does not apply to school district taxes. For example, if your home is assessed at $100,000, the first $25,000 is exempt from all taxes, and an additional $25,000 is exempt from non-school taxes, effectively lowering your taxable value significantly. This reduction in taxable value directly translates to lower property tax bills, which is a major benefit for families, retirees, and individuals who have chosen Florida as their permanent home.

The “Save Our Homes” (SOH) Amendment: In addition to the monetary exemption, the Homestead Exemption also includes the crucial “Save Our Homes” (SOH) amendment. The SOH amendment caps the annual increase in the assessed value of a homesteaded property at 3% or the percentage change in the Consumer Price Index (CPI), whichever is lower. This protection prevents rapid increases in property values from leading to exorbitant tax hikes, providing stability and predictability for homeowners’ budgets. Without SOH, a sudden surge in market values could make property ownership unaffordable for many long-term residents. This protection is a cornerstone of Florida property law, safeguarding the lifestyle and financial well-being of its permanent residents. It also provides peace of mind for those looking to stay in their homes long-term, enjoying the Florida climate and community.

Additional Exemptions for Specific Groups

Beyond the Homestead Exemption, Florida offers a variety of other property tax exemptions tailored to specific groups of individuals who meet certain criteria. These programs further demonstrate the state’s commitment to supporting its diverse population and making homeownership accessible and sustainable.

-

Veterans and Disabled Persons: Florida provides significant tax relief for veterans, particularly those with service-connected disabilities. The specific amount of exemption varies based on the percentage of disability. For example, a veteran with a 10% or more service-connected disability may receive a $5,000 exemption. Furthermore, totally and permanently disabled veterans, or those who are legally blind due to service-connected reasons, may be eligible for a total exemption from property taxes. Similar exemptions also extend to surviving spouses of veterans. These exemptions are a testament to the state’s respect for military service and its commitment to caring for those who have served.

-

Senior Citizens: Many counties in Florida offer additional property tax exemptions for qualified seniors who meet specific age and income requirements. These “senior exemptions” can further reduce the taxable value of their homesteaded property, providing crucial financial assistance to retirees living on fixed incomes. The exact criteria and amount of the exemption can vary by county, so it’s important for eligible seniors to check with their local Property Appraiser’s office. This support allows senior citizens to comfortably enjoy their retirement years in Florida, often attracting many to the state for its appealing climate and senior-friendly communities.

-

Blind Persons and Totally & Permanently Disabled Persons: Individuals who are legally blind or have a total and permanent disability, regardless of age, may be eligible for an additional property tax exemption. The amount of this exemption is usually a fixed sum that further reduces their taxable value. This assistance helps to alleviate some of the financial burdens associated with living with disabilities, ensuring a more comfortable lifestyle.

-

Widows and Widowers: Florida offers a $500 property tax exemption for widows and widowers. This exemption provides a small but meaningful reduction in tax liability during a challenging time, demonstrating the state’s support for grieving spouses.

-

First Responders and Active Military Personnel: In some cases, specific exemptions or deferral programs may be available for active military personnel deployed outside the U.S. or for certain first responders who become totally and permanently disabled in the line of duty. These programs aim to provide relief to those who serve and protect our communities and nation.

To apply for any of these exemptions, property owners must file an application with their County Property Appraiser’s office, typically by March 1st of the year for which they are seeking the exemption. It’s crucial to file on time and provide all necessary documentation. While the Homestead Exemption and SOH benefits are automatically renewed each year after the initial application, other exemptions might require periodic reapplication or verification. Understanding these opportunities is key to optimizing property ownership costs and ensuring a sustainable lifestyle in Florida, whether you’re a long-term resident or considering making the Sunshine State your permanent home.

Conclusion: Mastering Florida Real Estate Taxes for a Seamless Lifestyle

Understanding “When Are Florida Real Estate Taxes Due?” is far more than just knowing a few dates; it’s about mastering a crucial aspect of property ownership in one of the world’s most desirable destinations. From the excitement of choosing a vacation home in Orlando to the tranquility of a long-term stay near Tampa’s beaches, or the vibrant energy of a Miami investment, the Florida lifestyle is diverse and appealing. However, managing your property taxes effectively is fundamental to enjoying this lifestyle without financial strain or legal complications.

We’ve explored the annual cycle of Florida property taxes, beginning with the January 1st assessment, through the November 1st billing, and culminating in the March 31st payment deadline before delinquency sets in on April 1st. We’ve highlighted the substantial benefits of the early payment discount system, which can save property owners up to 4% by paying in November. Conversely, we’ve outlined the severe consequences of late payments, from accumulating interest and fees to the potential loss of property through tax lien and tax deed sales. Finally, we’ve delved into the valuable exemptions and relief programs available, particularly the transformative Homestead Exemption and the protective “Save Our Homes” amendment, alongside other specific exemptions for veterans, seniors, and disabled persons.

For current property owners, the message is clear: proactive management of your tax obligations is key. Mark your calendars, take advantage of the early payment discounts, and ensure you apply for any exemptions for which you qualify. For prospective buyers or those considering a long-term stay or investment in Florida real estate, gaining a thorough understanding of these tax principles is an essential step in your due diligence. Property taxes are a significant recurring expense, and factoring them into your budget from the outset will prevent future surprises and contribute to a more secure and enjoyable experience.

Ultimately, whether your connection to Florida is through travel, tourism, long-term accommodation, or as a proud homeowner, being informed about real estate taxes empowers you to make smarter financial decisions. This knowledge safeguards your investment, optimizes your budget, and allows you to fully embrace the unparalleled lifestyle and opportunities that the Sunshine State perpetually offers. So, stay informed, pay on time, and continue to savor every moment of your Florida experience.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.