The allure of the Sunshine State is undeniable. With its pristine beaches, vibrant cities, and world-class attractions, Florida draws millions of residents and tourists each year. From the magical theme parks of Orlando to the Art Deco splendor of Miami, and the cultural richness of Tampa, there’s a unique lifestyle awaiting every visitor and resident. However, beneath the sunny skies and swaying palm trees lies a persistent challenge for anyone hitting the road: shockingly high car insurance premiums. For many, the cost of auto insurance in Florida can feel like an additional hidden tax on the dream of living or vacationing here.

Understanding why your car insurance bill is significantly higher in Florida compared to other states requires a dive into a multifaceted issue, encompassing everything from the state’s unique demographics and booming tourism industry to its susceptibility to natural disasters, complex legal landscape, and even the evolving technology within our vehicles. Whether you’re a long-time resident, a recent transplant, or a “snowbird” enjoying a seasonal stay, unraveling these factors is crucial to navigating the roads of the Sunshine State with both enjoyment and financial prudence. This comprehensive guide will explore the primary drivers behind Florida’s elevated car insurance costs, offering insights into why this beautiful corner of the world comes with a premium on peace of mind behind the wheel.

The Sunshine State’s Unique Driving Landscape

Florida’s environment for drivers is unlike almost anywhere else in the United States, shaped by an intricate blend of rapid population growth, an unparalleled tourism sector, and a distinctive demographic makeup. These elements converge to create a high-traffic, high-risk scenario that directly impacts insurance premiums.

A Magnet for Millions: Population Density and Tourism

The sheer volume of people on Florida‘s roads is perhaps the most immediate factor contributing to higher insurance costs. As one of the fastest-growing states in the nation, Florida’s population has surged, leading to increased traffic density, particularly in major metropolitan areas and along key arteries. More cars on the road inevitably lead to a higher likelihood of accidents. Cities like Orlando, Miami, and Tampa are constantly buzzing with activity, translating into bumper-to-bumper traffic during peak hours and on weekends. This constant congestion not only increases the frequency of collisions but also raises the severity of them, as even minor fender-benders can escalate into significant claims given the volume of vehicles involved.

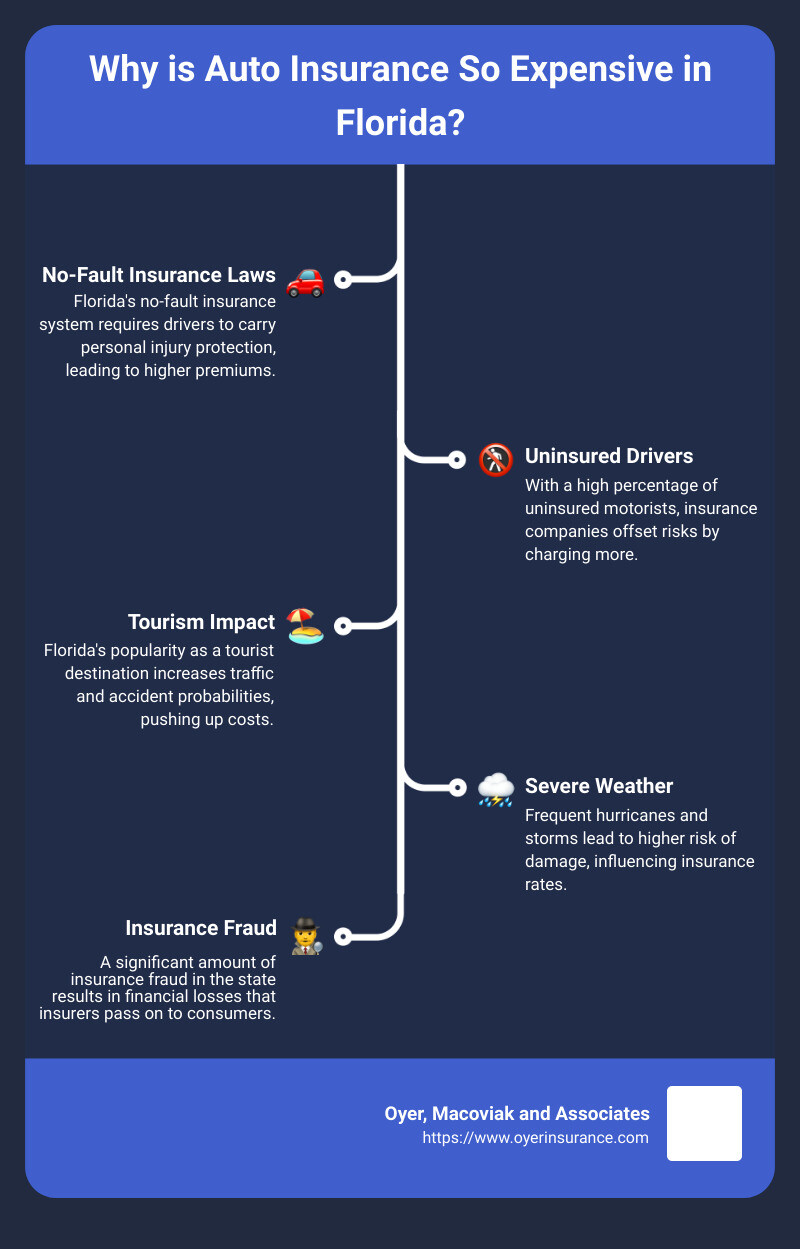

Beyond its permanent residents, Florida welcomes over 130 million tourists annually. These visitors, often unfamiliar with local road systems and potentially distracted by their travel plans, contribute significantly to the driving complexity. Many tourists rent vehicles, adding to the total number of cars on the road, and the nature of rental car insurance can also have ripple effects on the broader market. Whether they’re heading to the theme parks near Kissimmee, exploring the vibrant nightlife of South Beach, or relaxing on the pristine sands of Clearwater Beach, these temporary drivers introduce an element of unpredictability that insurance companies must factor into their risk assessments. The blend of daily commuters, commercial vehicles, and a constant influx of tourist traffic creates an environment ripe for accidents, driving up the baseline risk for all drivers in the state.

The Rhythms of Seasonal Residents and Retirees

Another defining characteristic of Florida’s driving landscape is its significant population of seasonal residents, famously known as “snowbirds,” and a large proportion of retirees. The arrival of snowbirds, typically from colder northern states or Canada, brings a substantial increase in vehicle presence during the winter months, particularly in popular retirement havens like Fort Myers, Naples, and Sarasota. These seasonal migrations lead to predictable surges in traffic, congestion, and consequently, accident rates in specific regions at specific times of the year. Insurance models must account for these seasonal fluctuations, understanding that a quiet beach town in July might become a bustling hub by January.

Furthermore, Florida boasts one of the highest percentages of residents aged 65 and over in the United States. While age is certainly not the sole determinant of driving ability, statistical data often indicates that drivers in certain older age brackets may have different accident profiles, sometimes involving slower reaction times or impaired vision, which can contribute to higher accident rates. Additionally, the medical costs associated with treating injuries for older individuals after an accident tend to be higher, further inflating insurance payouts. This demographic reality is a crucial component in how insurance companies calculate risk and set premiums across the state, ensuring they can cover potential claims in a population with a higher likelihood of incurring significant medical expenses post-collision.

Navigating Nature’s Fury: Weather and Environmental Challenges

Florida’s stunning natural beauty is intrinsically linked to its unique geography and climate, which unfortunately also expose the state to a host of environmental perils. These natural challenges, particularly its vulnerability to severe weather, play a substantial role in hiking up car insurance costs.

The Unpredictable Wrath of Hurricanes and Tropical Storms

Few states contend with the sheer power and frequency of severe weather events quite like Florida. Located in one of the most active hurricane basins in the world, the state is a prime target for tropical storms and hurricanes, especially during the Atlantic hurricane season from June to November. These events wreak havoc not just on homes and businesses but also on vehicles. Cars are highly susceptible to damage from high winds, flying debris, and most significantly, widespread flooding. A single major hurricane, like Hurricane Ian or Hurricane Andrew, can result in hundreds of thousands of damaged or totaled vehicles across vast areas, from the Panhandle to the Florida Keys.

The direct impact on vehicles from these storms includes shattered windows, dents from airborne objects, and severe water damage that can render a car irreparable. Water damage, in particular, is insidious, affecting a vehicle’s electrical system, engine, and interior, often leading to a total loss. Insurance companies must price in this catastrophic risk, building a substantial buffer into comprehensive coverage premiums to prepare for the massive claims payouts that follow such events. Coastal cities like Key West, Miami Beach, and Fort Lauderdale face particularly elevated risks due to their proximity to the ocean and susceptibility to storm surge. This consistent threat of natural disaster forms a fundamental part of the actuarial calculations that drive up insurance rates for all drivers in the state, even those living in less vulnerable inland areas, due to the interconnectedness of the state’s insurance market.

Beyond the Storms: Other Environmental Factors

While hurricanes grab the headlines, Florida faces other less dramatic but equally impactful environmental challenges that affect vehicles and, by extension, insurance costs. One unique geological phenomenon is the prevalence of sinkholes. Underlying much of Florida is porous limestone, which can dissolve over time, creating underground cavities. When the surface layer collapses, it forms a sinkhole, capable of swallowing cars, homes, and even entire sections of road. While less common than hurricane damage, sinkhole claims can be incredibly costly, often resulting in a total loss for vehicles that fall in. Areas such as Gainesville, Ocala, and parts of Tampa Bay are particularly prone to these geological events. Although specific sinkhole coverage is often an add-on, the underlying risk contributes to the overall premium landscape for comprehensive coverage.

Furthermore, Florida’s generally low elevation and high water table mean that even moderate rainfall can lead to localized flooding, especially in urban areas with inadequate drainage or near rivers and lakes. Flash floods can quickly submerge roads and vehicles, leading to water damage similar to that caused by storm surges. This constant low-level threat of water-related damage, combined with the more dramatic impact of hurricanes and tropical storms, ensures that vehicle owners in Florida are always paying a premium for comprehensive coverage that protects against the unpredictable and often destructive forces of nature. The sheer volume and diversity of environmental risks necessitate a higher financial buffer for insurers, which is ultimately passed on to policyholders.

The Financial and Legal Labyrinth of Florida’s Roads

Beyond traffic and natural disasters, the financial and legal frameworks governing auto insurance in Florida introduce additional layers of complexity and cost. From its unique no-fault system to the escalating expenses of modern vehicle repairs and the shadow of auto theft, these elements significantly contribute to the state’s high premiums.

Florida’s No-Fault System and Its Complications

Florida operates under a “no-fault” auto insurance system, which mandates that all drivers carry Personal Injury Protection (PIP) coverage. The original intent of PIP was to streamline the claims process, allowing injured parties to receive medical benefits and lost wages from their own insurer, regardless of who was at fault for an accident. This was meant to reduce litigation and speed up recovery. However, in practice, Florida’s no-fault system has become a significant driver of higher premiums, largely due to rampant fraud and inflated medical claims.

The system has unfortunately been exploited by some medical providers, clinics, and even unscrupulous attorneys who engage in “runners” to solicit accident victims, often encouraging unnecessary or exaggerated treatments. These fraudulent activities include billing for services never rendered, upcoding medical procedures, or performing excessive diagnostic tests. The average PIP claim in Florida is substantially higher than in many other states, directly impacting insurers’ loss ratios. Insurers are forced to absorb these costs, passing them on to all policyholders through higher premiums. Despite legislative efforts to curb PIP fraud, the problem persists, making the no-fault system a complex and costly component of Florida’s insurance market. The continuous legal battles surrounding PIP and bodily injury liability claims also contribute to higher legal expenses for insurers, which are ultimately reflected in policy costs.

The Rising Cost of Repairs and Replacement

The vehicles we drive today are marvels of engineering, packed with advanced technology designed for safety and convenience. However, this sophistication comes at a price, particularly when it comes to repairs after an accident. Modern cars are equipped with intricate sensor systems, cameras, radar, and lidar for features like adaptive cruise control, lane-keeping assist, and automatic emergency braking. A seemingly minor fender-bender that once only required replacing a bumper can now involve recalibrating expensive sensors embedded within that bumper, significantly increasing repair costs.

Furthermore, the materials used in vehicle construction, such as high-strength steel, aluminum alloys, and carbon fiber, require specialized tools and highly skilled technicians for repair, driving up labor costs. Parts themselves are more expensive and, due to global supply chain issues, can be harder to source, leading to longer repair times and potential rental car expenses for insurers. In a state like Florida, where a significant portion of the population enjoys a luxury lifestyle, the prevalence of high-end vehicles in areas like Palm Beach, Boca Raton, and Winter Park further inflates the average cost of repairs and replacements. A collision involving a premium vehicle can result in claims that are exponentially higher than those involving standard models, creating another upward pressure on overall insurance premiums across the state.

The Shadow of Auto Theft and Vandalism

While Florida may not always top the charts for auto theft compared to some other states, crime rates, particularly in densely populated urban areas, still contribute to insurance costs. Vehicle theft and vandalism are persistent issues that fall under comprehensive coverage, impacting premiums for all drivers. From opportunistic break-ins to organized theft rings targeting specific vehicle models or parts, these incidents lead to significant claims for stolen vehicles or damage repairs.

The presence of major international ports and proximity to various borders also makes Florida a potential transit point for stolen vehicles being shipped overseas, further incentivizing theft. Carjackings and catalytic converter thefts have also seen spikes in recent years, adding another layer of risk. Insurance companies analyze crime statistics by zip code, meaning that residents in areas with higher rates of vehicle theft or vandalism, such as certain neighborhoods in Jacksonville or St. Petersburg, will typically pay higher comprehensive premiums. The cost of replacing stolen vehicles or repairing vandalized ones represents a considerable expense for insurers, which, like all other risks, is ultimately absorbed into the premiums paid by policyholders across the state.

Mitigating the Costs: Strategies for Florida Drivers

While many factors driving up Florida car insurance premiums are beyond individual control, drivers are not entirely without options. By understanding their coverage needs and implementing smart shopping and driving strategies, residents can effectively navigate the high costs and find more affordable rates.

Smart Choices and Proactive Measures

The first and arguably most impactful step a Florida driver can take is to shop around extensively for insurance quotes. Premiums can vary wildly between different providers, sometimes by hundreds or even thousands of dollars for similar coverage. Utilizing online comparison tools and consulting with independent insurance agents who can access multiple carriers are excellent ways to compare rates from companies like State Farm, Geico, Progressive, and Allstate. Don’t settle for the first quote you receive.

Bundling policies is another highly effective strategy. Most insurance companies offer significant discounts when you combine your auto insurance with other policies, such as homeowners, renters, or even boat insurance. This not only simplifies your insurance management but can lead to substantial savings.

Maintaining a clean driving record is paramount in Florida. A history of accidents or traffic violations, particularly serious ones like DUIs, will dramatically increase your premiums for years. Driving safely and defensively, especially in the high-traffic, tourist-heavy environments of Florida, is the best way to keep your rates down. Participating in safe driver programs or taking defensive driving courses can sometimes also yield discounts.

Choosing higher deductibles for comprehensive and collision coverage can lower your monthly premiums, but it’s crucial to ensure you have enough savings to cover that deductible if you need to make a claim. Similarly, dropping unnecessary coverage for older vehicles might be an option. If your car is worth less than the cost of your collision and comprehensive deductibles combined, it might not be financially prudent to keep those coverages.

Finally, consider telematics programs. Many insurers offer devices or apps that monitor your driving habits (speed, braking, mileage). If you demonstrate safe driving behaviors, you could qualify for significant discounts. While it means sharing driving data, the potential savings can be considerable for cautious drivers.

Understanding Coverage Needs in the Sunshine State

Given Florida’s unique risks, it’s vital not only to find affordable insurance but also to ensure you have adequate coverage. While Florida’s minimum requirements are for PIP and Property Damage Liability, these bare minimums are often insufficient to protect you financially.

Bodily Injury Liability (BIL) is not required by state law unless you’ve had a prior incident, but it is highly recommended. In a state with a litigious environment and high medical costs, the minimal PIP coverage (typically $10,000) is quickly exhausted. If you are at fault for an accident and someone else is injured, BIL coverage protects your assets from lawsuits by paying for their medical expenses, lost wages, and pain and suffering beyond what their PIP covers. Given the high medical costs, policies with at least $100,000 per person and $300,000 per accident are often advised.

Uninsured/Underinsured Motorist (UM/UIM) coverage is another critical consideration. Despite high insurance costs, many Florida drivers are uninsured or carry only minimum coverage. If you’re hit by one of these drivers, UM/UIM protects you by covering your medical bills and lost wages up to your policy limits, similar to what BIL would cover for others if you were at fault.

For comprehensive protection against natural disasters, theft, and vandalism, Comprehensive and Collision coverage are essential, especially given Florida’s hurricane risk. While these are optional if your vehicle is paid off, they are non-negotiable for anyone with a car loan or lease.

Finally, consider an umbrella policy. Given the potential for large liability claims in Florida, an umbrella policy provides additional liability coverage beyond the limits of your auto and homeowners policies, offering an extra layer of protection for your assets against severe lawsuits. By carefully assessing these options and making informed choices, Florida drivers can secure adequate protection without overspending.

Conclusion

The question of “Why is Florida car insurance so expensive?” leads to a complex answer, intertwining a unique blend of geographical, demographic, legal, and economic factors. From the relentless surge of population growth and tourism that congests our roads, to the annual dance with devastating hurricanes and the ever-present threat of sinkholes, the environmental risks alone demand a significant premium. Add to this the intricacies of a no-fault system plagued by fraud, the escalating costs of repairing technologically advanced vehicles, and the persistent issue of auto theft, and it becomes clear why insurers must price their policies higher to maintain solvency in the Sunshine State.

While these challenges present a formidable hurdle for drivers, they also underscore the critical importance of comprehensive and well-understood auto insurance. Despite the higher costs, having robust coverage is not merely a legal requirement but an essential safeguard for your financial well-being, offering peace of mind amidst the unpredictable nature of Florida’s roads. By actively seeking competitive quotes, bundling policies, maintaining an impeccable driving record, and judiciously selecting appropriate coverage levels, Florida residents can exert some control over their insurance expenditures.

Ultimately, the vibrancy and appeal of Florida – its stunning landscapes, world-renowned attractions, and unique lifestyle – continue to draw people from across the globe. Navigating its roads requires not just a good sense of direction, but also an informed approach to car insurance, ensuring that the dream of living or vacationing in this dynamic state remains financially sustainable and enjoyable for all.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.