Florida, often lauded as the Sunshine State, beckons millions of visitors each year with its sun-drenched beaches, world-class theme parks, and vibrant cultural tapestry. Whether you’re planning a family vacation to Orlando to experience the magic of Walt Disney World and Universal Studios Florida, a relaxed getaway to the pristine shores of Clearwater Beach, or an exploration of the unique ecosystems of the Everglades National Park, a car often becomes an indispensable companion for navigating the vast expanse of this diverse state. However, before you buckle up and hit the open road, a crucial question arises for any visitor: “Do you have to have car insurance in Florida?” While this question might seem straightforward, understanding the nuances surrounding non-resident drivers and their insurance requirements is vital for a smooth and legal journey through the Sunshine State.

This article delves into the specific regulations and considerations for visitors driving in Florida, focusing on whether car insurance is a mandatory requirement for those not residing within the state. We will explore the general legal landscape of car insurance in Florida, the implications for tourists, and practical advice to ensure you are compliant and protected while enjoying all that Florida has to offer.

Understanding Florida’s Financial Responsibility Law

Florida operates under a system that mandates drivers demonstrate financial responsibility to cover damages they might cause in an accident. This law is designed to protect individuals involved in collisions by ensuring that those at fault can compensate for medical expenses, property damage, and other related costs. For Florida residents, this typically translates into mandatory insurance coverage. However, the application of these laws to non-residents, particularly those visiting on a temporary basis, requires a closer look.

The Core Requirement: Bodily Injury and Property Damage Liability

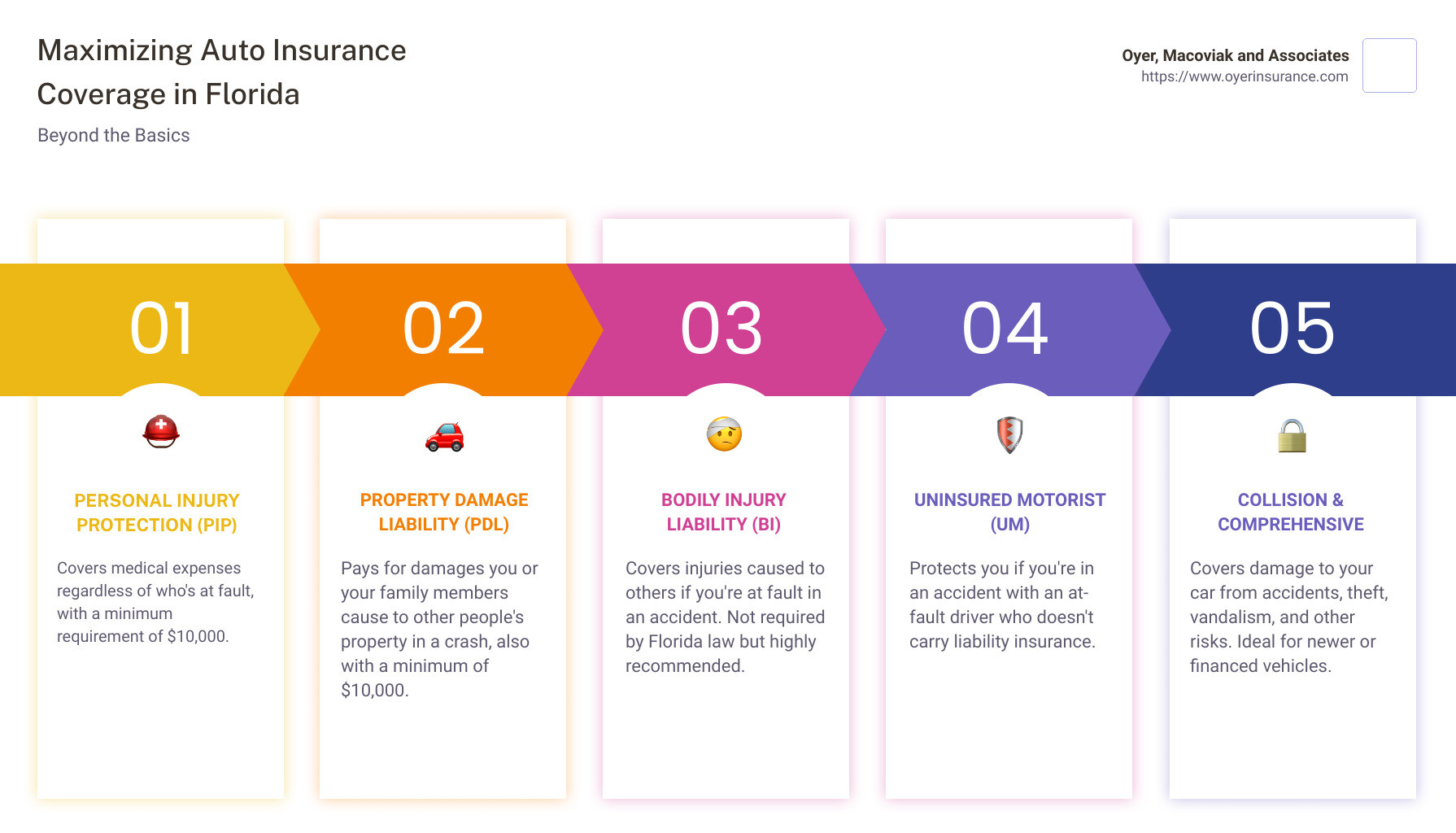

At its heart, Florida’s Financial Responsibility Law requires that all drivers carry a minimum amount of Bodily Injury Liability (BIL) and Property Damage Liability (PDL) insurance. These coverages are crucial because they provide a financial safety net should you be found responsible for causing an accident.

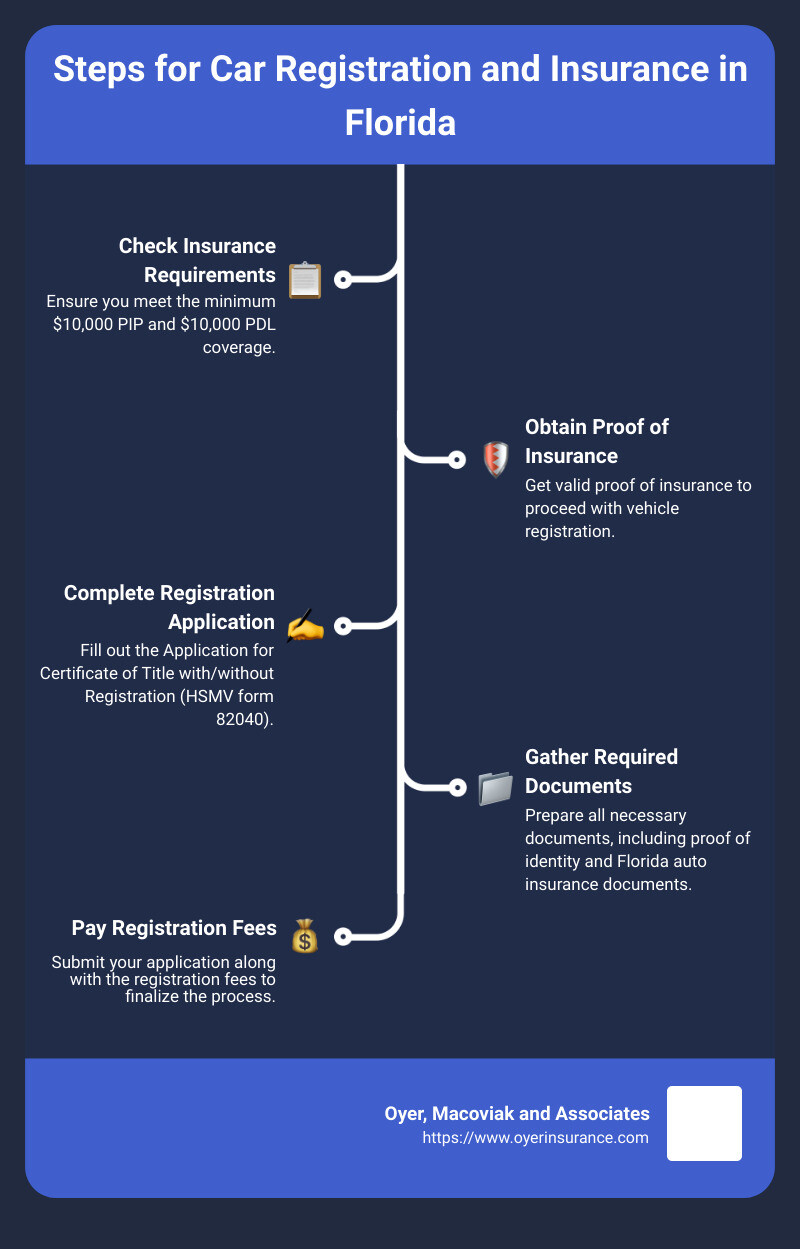

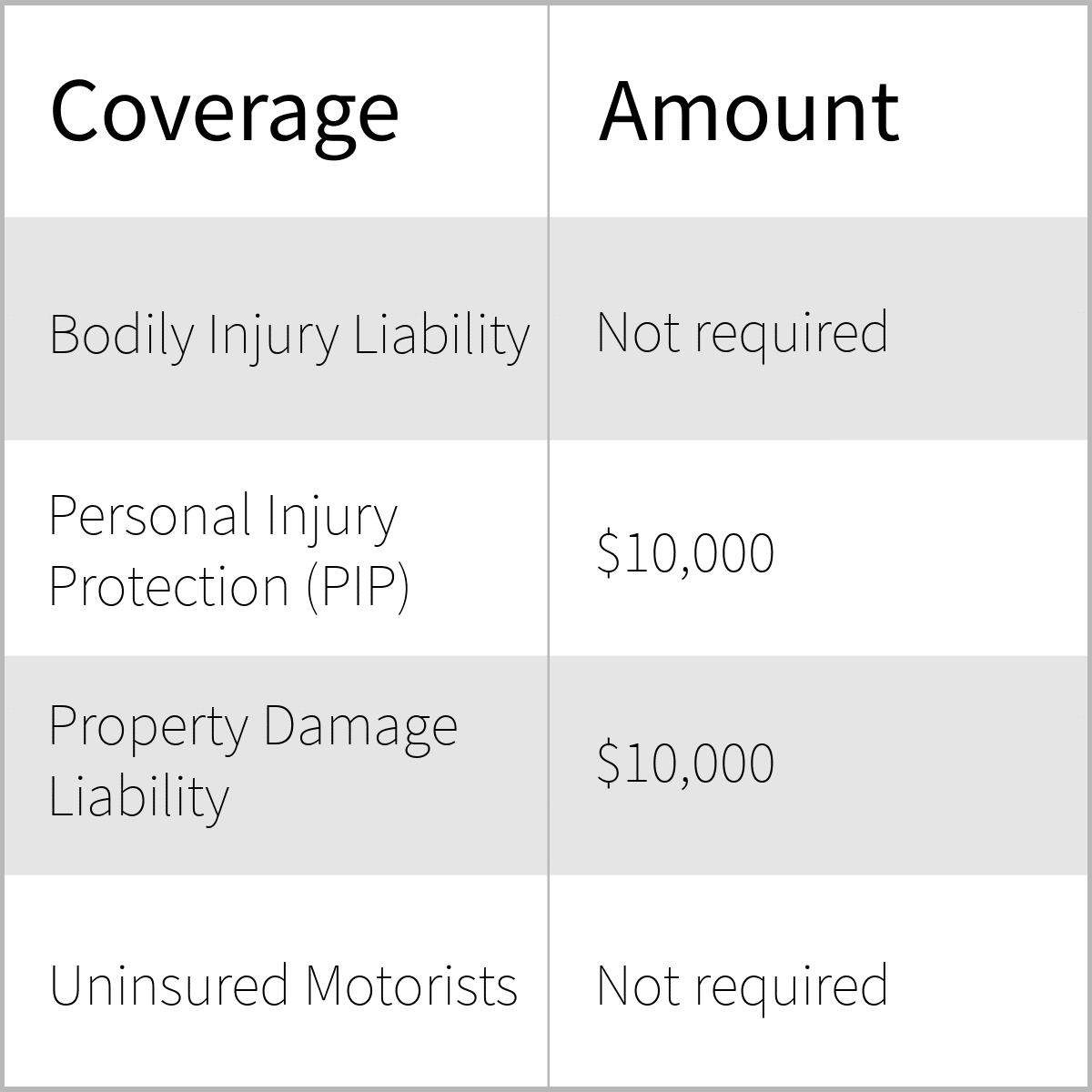

- Bodily Injury Liability (BIL): This coverage helps pay for the medical expenses, lost wages, and pain and suffering of others if you injure them in an accident. Florida law requires a minimum of $10,000 of BIL coverage per person and $20,000 per accident. This means that if you injure one person in an accident, your BIL coverage will pay up to $10,000 for their injuries. If you injure multiple people, your coverage is capped at $20,000 for all injuries in that accident.

- Property Damage Liability (PDL): This coverage assists in paying for the damage you cause to another person’s property in an accident, most commonly their vehicle. Florida law requires a minimum of $10,000 of PDL coverage per accident. This means if you are at fault and damage someone else’s car or other property, your PDL coverage will pay up to $10,000 for those repairs or replacement costs.

Personal Injury Protection (PIP) – A Unique Florida Mandate

Beyond BIL and PDL, Florida is one of the few states that historically mandated Personal Injury Protection (PIP) coverage for all registered vehicles. PIP is a “no-fault” coverage, meaning it pays for your own medical expenses and lost wages if you are injured in a car accident, regardless of who is at fault.

- PIP Coverage: Florida law requires a minimum of $10,000 in PIP coverage. This coverage is intended to expedite the payment of medical bills and lost wages without the need to determine fault immediately. It also typically covers up to 80% of necessary medical expenses and 60% of lost wages. It’s important to note that Florida has recently passed legislation to move away from a pure PIP system, with changes to PIP requirements and the introduction of a new tort option starting January 1, 2025. However, for the current period and for visitors, understanding the existing PIP landscape is still relevant.

Navigating Insurance Requirements as a Non-Resident Visitor

For tourists and short-term visitors to Florida, the question of whether they personally need to secure Florida-specific car insurance is often a point of confusion. The general rule of thumb is that if you are operating a vehicle legally registered in your home state or country and it carries the minimum required insurance coverage by that jurisdiction, you are typically covered when driving in Florida, provided your home state’s coverage meets or exceeds Florida’s minimums.

Reciprocity and Out-of-State Coverage

Florida, like most states, operates under a system of reciprocity. This means that if your home state has its own mandatory car insurance laws, and you are in compliance with those laws, your insurance policy is generally recognized as valid in Florida. The crucial aspect here is that your existing policy must offer coverage that is at least equivalent to Florida’s minimum requirements.

- Minimum Coverage Comparison: If your home state has lower minimum coverage requirements than Florida’s $10,000 BIL per person, $20,000 BIL per accident, and $10,000 PDL, you might be underinsured when driving in Florida. In such scenarios, your insurance company’s policy terms will dictate how it handles claims that exceed your home state’s limits but fall short of Florida’s.

- Rental Cars: When renting a car in Florida, rental companies are legally required to provide vehicles with the minimum state-required insurance coverage. However, this coverage might be basic and may not offer adequate protection for your needs. Many visitors opt to purchase additional insurance from the rental company or rely on their personal auto insurance policy, or even credit card benefits, to supplement this coverage. It is highly advisable to review your rental agreement carefully and understand the insurance options presented.

What Happens If You Don’t Have Adequate Coverage?

Driving in Florida without meeting the state’s financial responsibility requirements, whether as a resident or a non-resident operator of a vehicle, can lead to serious consequences. These can range from significant fines and penalties to the suspension of your driving privileges within the state.

- Penalties for Non-Compliance: If you are involved in an accident and cannot prove financial responsibility (i.e., valid insurance coverage that meets Florida’s minimums), you could face penalties including fines, the suspension of your driver’s license, and the impoundment of your vehicle. For visitors, this could lead to a disrupted trip and significant financial and legal complications.

- The Role of Your Personal Policy: Your personal auto insurance policy purchased in your home state is your primary line of defense. It’s essential to contact your insurance provider before your trip to confirm that your policy extends coverage to Florida and that it meets or exceeds the state’s minimum liability requirements. Some policies may have geographical limitations or different coverage levels when driving outside your home state.

Practical Tips for Visitors Driving in Florida

To ensure a hassle-free experience while driving in Florida, it’s prudent to take proactive steps regarding your car insurance. Being prepared can save you from unexpected financial burdens and legal entanglements.

Verifying Your Coverage Before You Travel

The most critical step for any visitor planning to drive in Florida is to understand their current insurance situation. This isn’t just about having a policy; it’s about having the right policy for the state you’ll be driving in.

- Contact Your Insurance Agent: Reach out to your insurance agent or company well in advance of your trip. Specifically ask them to confirm:

- Whether your current policy provides coverage in Florida.

- What are the minimum liability limits (BIL and PDL) your policy provides in Florida.

- Whether your policy includes PIP coverage, and if so, what are its limits and how it operates.

- What steps you should take if your current coverage is insufficient.

- Understand Rental Car Insurance Options: If you are renting a car, thoroughly investigate the insurance options offered by the rental agency. Consider:

- Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW): This is not insurance but a waiver that releases you from financial responsibility for damage to the rental car.

- Supplemental Liability Insurance (SLI): This increases the liability coverage beyond what is offered by the rental company’s basic coverage and your own policy.

- Personal Accident Insurance (PAI) and Personal Effects Coverage (PEC): These cover medical expenses for you and your passengers, and theft of personal belongings from the rental car, respectively.

- Your Credit Card Benefits: Some credit cards offer rental car insurance as a perk. Check your card’s benefits guide, but be aware that these often act as secondary coverage and may have limitations.

Carrying Proof of Insurance

Regardless of whether you are driving your own vehicle or a rental, always carry proof of insurance in your vehicle. This is a legal requirement in Florida.

- Physical or Digital Proof: This proof can be a physical insurance card provided by your insurance company or a digital version accessible via your insurer’s app or online portal. When driving a rental car, the vehicle will typically have its own proof of insurance documentation.

- Key Information to Have: Ensure your proof of insurance includes your name, the insurance company’s name, the policy number, the coverage period, and the vehicle’s identification number (VIN).

Considering Supplemental Coverage for Peace of Mind

While Florida law might recognize out-of-state insurance that meets minimums, it is often wise for visitors to consider enhancing their coverage for greater peace of mind, especially when exploring popular destinations like Miami, Tampa, or enjoying the beaches around Fort Lauderdale.

- Understanding Liability Limits: The minimum liability limits in Florida are relatively low. A serious accident can easily exceed these amounts, leaving you personally responsible for the remaining damages. If your home state’s minimums are also low, purchasing supplemental liability insurance, either through your personal policy or the rental car company, can be a wise investment.

- Comprehensive and Collision Coverage: If you are driving your own vehicle, ensure it has comprehensive and collision coverage if you wish to protect it against damage from accidents, theft, or other unforeseen events. If you are renting, understand the implications of declining the rental company’s CDW/LDW and ensure your personal insurance or credit card benefits adequately cover the rental vehicle.

In conclusion, while Florida does not require non-residents to obtain a separate Florida car insurance policy for temporary visits, it unequivocally requires all drivers operating vehicles within its borders to demonstrate financial responsibility. This means ensuring that your existing auto insurance, whether from your home state or through a rental agreement, meets or exceeds the state’s minimum liability requirements for bodily injury and property damage. By taking the time to understand these requirements and verifying your coverage before you embark on your Floridian adventure, you can drive with confidence and focus on enjoying the many wonders this beautiful state has to offer.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.