The Golden State of California has long captivated imaginations, drawing visitors and prospective residents alike with its breathtaking natural beauty, innovative spirit, and diverse cultural tapestry. From the sun-drenched beaches of San Diego to the majestic redwoods of the north, and from the vibrant urban pulse of Los Angeles to the iconic cable cars of San Francisco, California offers an unparalleled lifestyle. Many dream of making this dynamic state their home, whether for a temporary escape, a luxury retreat, or a permanent relocation, often acquiring property or establishing a business here. With such significant life and investment decisions, particularly concerning property and assets, questions about wealth transfer and legacy planning naturally arise. One of the most common inquiries, especially for those considering California for its lifestyle and investment potential, is: “Does California have an inheritance tax?” The answer, which provides a significant advantage for those looking to build a legacy in this desirable region, is no. California does not impose a state-level inheritance tax, nor does it levy a state-level estate tax.

This absence of state-specific death taxes positions California favorably compared to a handful of other states that do impose such levies. For individuals and families who own property in the state—be it a charming Airbnb investment property in Palm Springs, a sprawling family estate overlooking the Pacific Ocean, or a vibrant boutique hotel in Napa Valley—this is often a welcome relief. It simplifies the process of passing on wealth and assets to heirs, allowing them to fully enjoy the inheritance without the additional burden of a state tax. While this news is certainly positive, it’s crucial to understand that while California does not have its own inheritance or estate tax, other considerations and potential federal taxes still come into play when planning for the future of your assets in this beautiful state.

Navigating Wealth Transfer in the Golden State

Understanding the nuances of wealth transfer is a vital component of smart financial and lifestyle planning, especially for those whose lives or investments are intertwined with California. Whether you’re considering purchasing a vacation home in Lake Tahoe, investing in a hotel development project in Orange County, or simply enjoying the unparalleled lifestyle the state offers, knowing the landscape of estate laws is essential.

The Golden State’s Stance on Inheritance

As confirmed, California stands as one of the majority of U.S. states that have opted not to impose an inheritance tax on beneficiaries or an estate tax on the deceased’s estate at the state level. This policy significantly reduces the tax burden on inheritors of California property, assets, or businesses. For instance, if you’ve invested in a luxury hotel suite in Beverly Hills or developed a unique travel experience company headquartered in Silicon Valley, your heirs would not face state-level inheritance taxes when those assets are passed down.

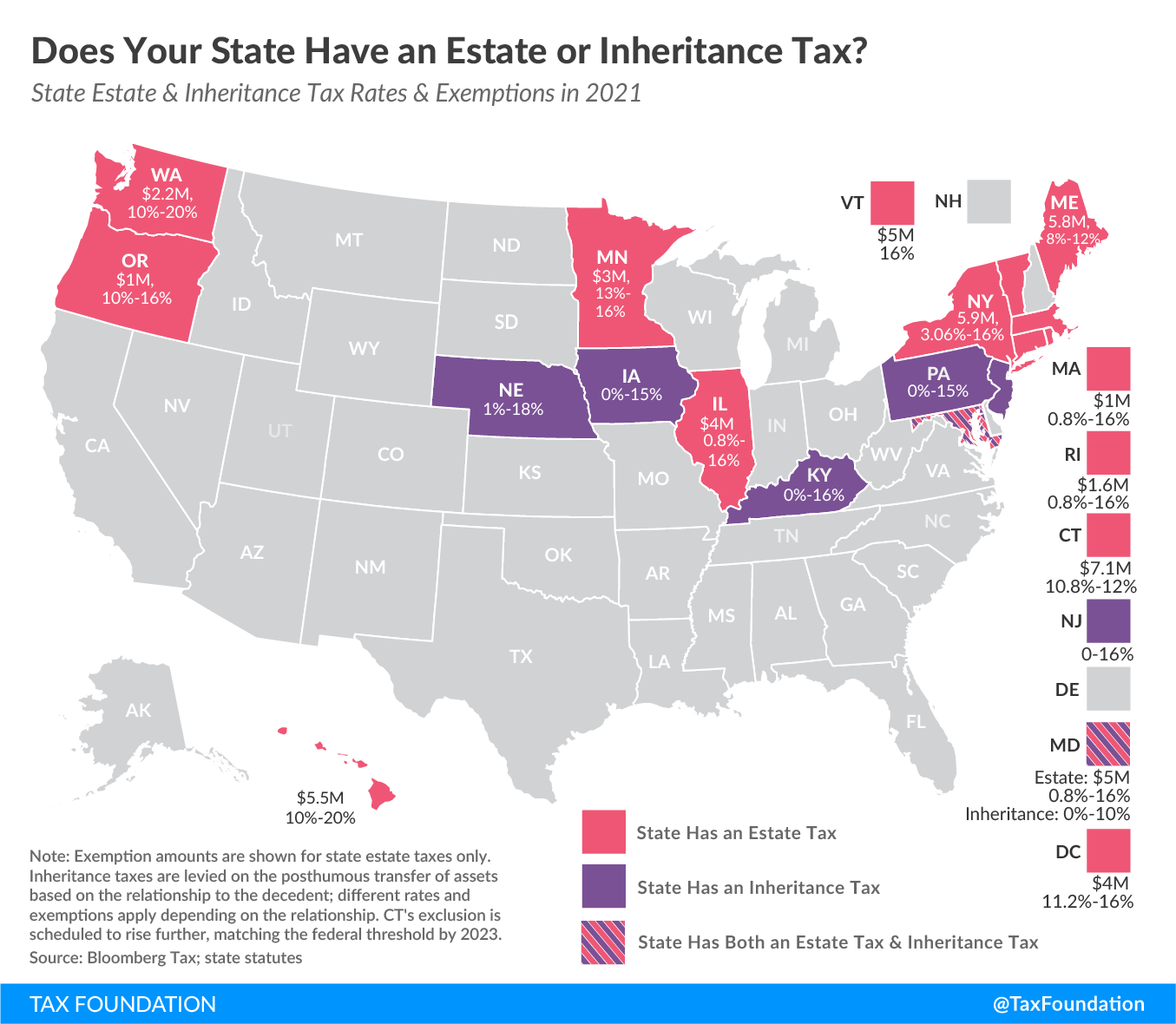

This contrasts with a handful of states that do have an inheritance tax, which is typically paid by the person receiving the inheritance. These states include Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. Similarly, some states levy a state estate tax, which is paid from the deceased person’s estate before assets are distributed to heirs. These estate tax states include Connecticut, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, Washington, and the District of Columbia. California’s absence from both of these lists makes it an attractive place for those looking to preserve their legacy with fewer state-level tax implications.

Federal Estate Tax: A Key Consideration

While California provides a reprieve from state-specific death taxes, it’s paramount to remember that the US Federal Estate Tax still applies to eligible estates. This tax, levied by the federal government, is imposed on the transfer of a deceased person’s taxable estate, which includes everything the person owned or had certain interests in at the time of death. The threshold for this tax is quite high, meaning it typically affects only very wealthy individuals. For example, for 2024, the federal estate tax exemption is $13.61 million per individual. This means that an individual’s estate must exceed this substantial amount to be subject to the federal estate tax. For married couples, this exemption is effectively doubled, allowing for even greater tax-free transfers.

Understanding this distinction is crucial for estate planning, especially for those with significant assets in California. The federal estate tax is administered by the IRS (Internal Revenue Service), and while it can be a significant concern for large estates, many California residents and property owners will find their estates fall well below the federal exemption limits. Furthermore, the federal estate tax has a concept called “portability,” which allows a surviving spouse to use any unused portion of their deceased spouse’s federal estate tax exemption. This provides even more flexibility for families planning their wealth transfer strategies, potentially shielding a larger combined estate from federal taxation.

Understanding Probate in California

Beyond taxes, another critical aspect of wealth transfer in California that profoundly impacts beneficiaries and the overall timeline of inheriting assets is the probate process. Probate is a legal, court-supervised process that verifies a deceased person’s will (if one exists), identifies and inventories their property, pays their debts and taxes, and finally distributes their remaining assets to the appropriate heirs. While the California lifestyle often emphasizes ease and enjoyment, the probate process can unfortunately be anything but.

The Probate Journey: Lengthy and Costly

In California, probate is generally required when a person dies owning assets in their individual name that exceed a certain value (currently $184,500 for deaths in 2022 and later) and that are not held in a trust or through other non-probate transfer mechanisms. If a will exists, the Probate Court will validate it. If there is no will, the estate will be distributed according to California Probate Code intestacy laws.

The major downsides of probate in California are its duration and expense. It is a notoriously lengthy process, often taking anywhere from nine months to two years, and sometimes even longer for complex estates. This extended timeline can be particularly frustrating for heirs, especially if they are looking to sell an inherited property, such as a San Francisco apartment or a Palm Springs vacation rental, or if they depend on inherited funds for their financial planning.

Furthermore, probate can be expensive. Costs typically include court filing fees, appraisal fees, and significant attorney and executor fees, all of which are statutory in California and calculated as a percentage of the gross estate value. These fees can quickly accumulate, diminishing the value of the inheritance that ultimately reaches the beneficiaries. For example, if an estate includes a valuable piece of real estate in Laguna Beach, even with no mortgage, its full market value contributes to the gross estate from which these fees are calculated.

When Probate Can Be Avoided

Fortunately, not all assets are subject to the California probate process. Certain assets can bypass probate, significantly streamlining the wealth transfer process:

- Assets held in a Living Trust: This is arguably the most effective way to avoid probate. Property transferred into a Living Trust can be distributed by the successor trustee without court involvement.

- Joint Tenancy with Right of Survivorship: Property owned in this manner (common for real estate between spouses) automatically passes to the surviving owner upon the death of the other, outside of probate.

- Assets with Beneficiary Designations: Accounts such as life insurance policies, 401(k)s, IRAs, and payable-on-death (POD) or transfer-on-death (TOD) bank and brokerage accounts transfer directly to the named beneficiaries, bypassing probate.

- Small Estates: California offers a simplified “small estate affidavit” procedure for estates below the aforementioned statutory threshold, allowing for the transfer of assets without full probate.

- Community Property with Right of Survivorship: Similar to joint tenancy, this allows a surviving spouse to directly inherit their deceased spouse’s share of community property.

For those planning their legacy in California, understanding these probate exceptions is crucial, as they offer pathways to ensure assets are transferred efficiently and cost-effectively, preserving more for loved ones.

Planning Your California Future: Property, Travel, and Estate Considerations

Given the absence of state inheritance or estate taxes and the complexities of probate in California, proactive estate planning is not just advisable; it’s essential for anyone with significant ties to the state. This is particularly true for individuals who own valuable properties, have business interests in the booming tourism or tech sectors, or simply wish to ensure their loved ones can easily navigate the transfer of wealth, allowing them to focus on grieving rather than bureaucratic hurdles.

Strategic Estate Planning for Your Heirs

Effective estate planning goes beyond simply drafting a will. It involves a comprehensive strategy designed to protect assets, minimize taxes, avoid probate, and ensure your wishes are carried out precisely.

-

Utilizing Trusts: Trusts are powerful tools in California estate planning.

- Revocable Living Trust: This is the cornerstone of many California estate plans. You transfer ownership of your assets (real estate, bank accounts, investments, businesses) into the trust while you are alive, and you typically serve as the trustee. Upon your death, a designated successor trustee distributes the assets to your beneficiaries according to your instructions, completely bypassing probate. This is immensely beneficial for someone who owns multiple properties, perhaps a primary residence, a vacation rental in Big Sur, and a commercial property in Hollywood.

- Irrevocable Trust: Unlike a Revocable Trust, assets placed in an Irrevocable Trust cannot be easily changed or withdrawn by the grantor. While less flexible, these trusts offer significant benefits for estate tax planning (removing assets from the taxable estate), asset protection, and qualifying for certain government benefits like Medi-Cal.

- Special Needs Trusts: For families with beneficiaries who have disabilities, a special needs trust can provide for their financial well-being without jeopardizing their eligibility for public assistance programs.

-

Beneficiary Designations: Regularly review and update beneficiary designations on all eligible accounts, including life insurance policies, retirement accounts (401(k)s, IRAs), and annuities. These designations override a will and ensure funds are distributed directly to your chosen heirs, bypassing probate.

-

Gifting Strategies: For individuals with very large estates approaching or exceeding the federal estate tax exemption, strategic gifting during their lifetime can reduce the taxable estate. The IRS allows for annual exclusion gifts (currently $18,000 per recipient per year in 2024) without incurring gift tax.

-

Business Succession Planning: For entrepreneurs and business owners in California’s dynamic economy, a robust business succession plan is vital. This ensures a smooth transition of leadership and ownership, whether it’s a boutique hotel chain, a travel tech startup, or a vineyard in Sonoma. Tools like Limited Liability Companies (LLCs) or Family Limited Partnerships (FLPs) can be used to manage and transfer business interests efficiently.

-

Specialized Trusts for Specific Assets:

- Qualified Personal Residence Trust (QPRT): Allows you to transfer your home into a trust while retaining the right to live there for a specified term, potentially reducing its value for estate tax purposes. This can be appealing for owners of high-value California real estate.

- Grantor Retained Annuity Trust (GRAT): An irrevocable trust used to transfer appreciating assets to beneficiaries with minimal gift and estate tax consequences.

- Charitable Remainder Trust (CRT): Allows you to donate assets to a charity while receiving income from the trust for a period, with the remaining assets going to the charity upon your death. This is often appealing for philanthropically minded individuals who want to leave a legacy while enjoying the vibrant California lifestyle.

The Impact on California Property and Investments

For those with a deep connection to California through property or investment in its thriving sectors (like tourism, hospitality, or real estate), estate planning takes on added significance. Owning a vacation property in Santa Barbara, an apartment building in Oakland, or a share in a popular resort near Yosemite National Park means these valuable assets must be properly managed for future transfer. Without proper planning, these assets could be tied up in probate for an extended period, preventing heirs from utilizing, selling, or continuing to develop them, potentially disrupting income streams from rentals or business operations.

Another important California-specific consideration is Medi-Cal Recovery. If a deceased individual received Medi-Cal benefits (California’s Medicaid program) after age 55, the state’s Department of Health Care Services is legally obligated to recover the cost of those benefits from the individual’s estate. This includes assets like homes, which might otherwise be passed down to heirs. Strategic planning, often involving Irrevocable Trusts or other asset protection strategies, can help protect assets from Medi-Cal Recovery while still ensuring the individual receives necessary care.

Making Informed Decisions for Your California Dream

The allure of California is undeniable. From its world-renowned landmarks like the Golden Gate Bridge and the Hollywood Sign, to its luxury resorts and diverse cultural experiences, it represents a dream for many. Whether you envision retiring here, establishing a new life, or investing in its booming economy, the state offers countless opportunities. However, realizing this dream also means making informed decisions about your financial future and legacy.

While California’s lack of state-level inheritance or estate taxes provides a significant advantage, the complexities of federal estate tax (for larger estates), the probate process, and other state-specific rules like Medi-Cal Recovery underscore the importance of comprehensive estate planning. For those who have embraced the California lifestyle and accumulated assets here, working with an experienced estate planning attorney and financial advisor is not merely a recommendation; it’s a necessity. These professionals can help you navigate the legal landscape, implement strategies like Living Trusts and proper beneficiary designations, and ensure your wealth is transferred to your loved ones efficiently and according to your wishes, preserving your legacy in the Golden State for generations to come. Ultimately, thoughtful planning ensures that your California dream extends far beyond your lifetime, securing the future for those you care about most, allowing them to continue to enjoy the fruits of your hard work and the enduring charm of this remarkable destination.