California, a state synonymous with dreams, innovation, and unparalleled beauty, beckons millions of travelers and aspiring residents each year. From the sun-kissed beaches of Malibu to the majestic peaks of Yosemite National Park, and the vibrant cityscapes of Los Angeles and San Francisco, the Golden State offers an intoxicating blend of experiences. Whether you’re planning a luxurious lifestyle escape, considering a long-term accommodation in a scenic locale, or contemplating investment in the thriving tourism sector through hotels or vacation rentals, understanding the local economic landscape is paramount. A crucial element of this landscape, often shrouded in complexity, is the property tax rate.

For anyone looking to buy property, invest in hospitality, or even just gain a deeper understanding of what drives the cost of living and business in this iconic state, comprehending California’s unique property tax system is essential. Unlike many other states, California’s property tax structure is largely defined by a historical ballot initiative, Proposition 13, which has shaped its real estate market for decades. This article delves into the intricacies of California’s property tax, exploring not just the rates but also their implications for travelers, potential homeowners, and investors in the state’s vibrant travel and hospitality industry.

Deciphering California’s Property Tax System: Proposition 13 and Beyond

At the core of California’s property tax framework lies Proposition 13, a landmark amendment passed in 1978. This proposition fundamentally altered how real estate is assessed and taxed, creating a system that is both unique and, at times, perplexing for those unfamiliar with its provisions. For anyone considering a permanent move, investing in a vacation home, or even developing a new resort, grasping Proposition 13 is the first step.

The primary effect of Proposition 13 is the establishment of a base property tax rate of 1% of the property’s assessed value. This rate is applied uniformly across all counties in California. However, what makes this system distinct is how the assessed value is determined and subsequently adjusted.

The Foundation: Assessed Value and Annual Increases

Under Proposition 13, a property’s assessed value is generally set at its fair market value at the time it was last purchased or changed ownership. This is a critical distinction from systems in other states where properties might be reassessed to market value annually or biennially. In California, once an assessed value is established, it can only increase by a maximum of 2% per year, regardless of how much the property’s actual market value may appreciate. This annual cap on increases provides a significant level of predictability and protection for long-term property owners against rapidly escalating tax bills.

However, this 2% cap is not absolute. The assessed value is fully reassessed to its current market value when there is a change in ownership. This means that when a property is sold, inherited (with some exceptions), or transferred, the new owner’s tax bill will be based on the new purchase price, effectively resetting the tax clock. This mechanism is crucial for understanding the dynamic nature of property taxes in California – older properties that haven’t changed hands in decades might have significantly lower tax bills compared to newly purchased, similarly valued properties in the same neighborhood. This disparity can sometimes lead to discussions about equity and fairness, but it remains a foundational aspect of the state’s property tax system.

Beyond the 1%: Understanding Local Assessments and Fees

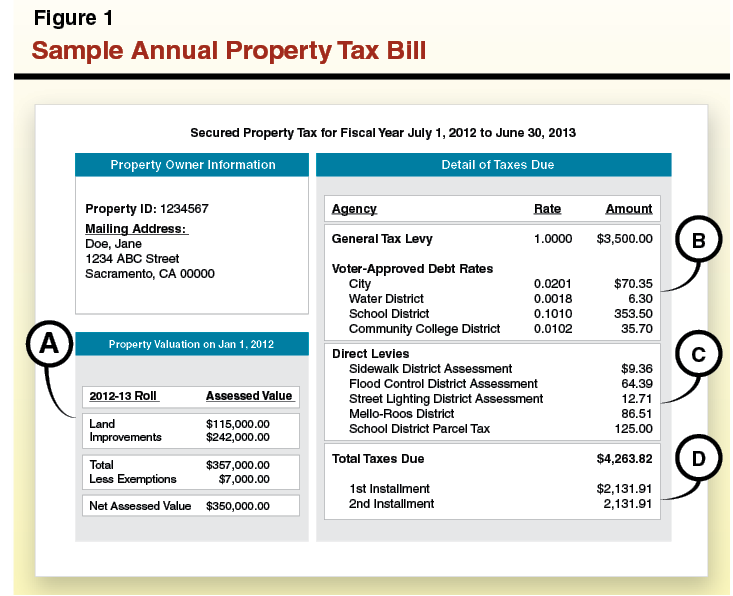

While Proposition 13 sets the base tax rate at 1%, the actual property tax bill often exceeds this figure due to various local assessments and direct levies. These additional charges are crucial for funding local public services and infrastructure projects, and they contribute significantly to the total effective tax rate.

These additional assessments can include:

- Voter-Approved Bonds: Many communities, from bustling cities to serene Napa Valley towns, pass bond measures to fund specific projects such as new schools, libraries, parks, or public safety improvements. The cost of these bonds is then levied on local property owners.

- Mello-Roos Community Facilities Districts (CFDs): These are particularly relevant for newer developments and planned communities. Mello-Roos districts are formed to finance major infrastructure projects like roads, sewers, schools, and fire stations that serve the new development. Property owners within these districts pay a special tax that can be substantial and significantly increase the overall property tax burden. For those considering buying a modern villa or a contemporary hotel in an emerging area like Ventura, understanding Mello-Roos taxes is non-negotiable.

- Direct Assessments: These are often levied for specific services like street lighting, landscape maintenance, or trash collection. While generally smaller than bond measures or Mello-Roos taxes, they still add to the total.

Consequently, while the base rate is 1%, the effective property tax rate in California can range from approximately 1.1% to 1.5% or even higher in areas with significant local assessments, especially in newer communities. It’s not uncommon for properties in areas like Orange County or parts of Riverside County with new developments to see effective rates closer to 1.5% to 2% due to Mello-Roos and other special assessments.

Property Taxes and the California Lifestyle: What Travelers and Investors Need to Know

The unique property tax structure in California has far-reaching implications, not just for residents but also for the state’s dynamic travel industry, its diverse accommodation options, and the general lifestyle experienced by millions. For tourists considering long-term stays, digital nomads eyeing a temporary home, or investors looking at the hospitality sector, these tax considerations are integral to budgeting and strategic planning.

Impact on Residential Real Estate and Accommodation Choices

The property tax system directly influences the cost of housing and, by extension, the availability and pricing of various accommodation types. In high-demand areas like Beverly Hills, Santa Monica Pier adjacent communities, or the scenic coastline of Big Sur, property values are exceptionally high. While Proposition 13 caps annual tax increases for existing owners, new buyers face taxes based on the full purchase price. This contributes to the state’s reputation for high housing costs.

For travelers seeking alternative accommodations beyond traditional hotels or resorts, such as vacation rentals or long-term apartment leases, property taxes indirectly affect pricing. Property owners incorporate these costs into their rental rates, especially for premium villas or luxury suites in Palm Springs or San Diego. This means that a significant portion of what a traveler pays for a short-term rental helps cover the owner’s property tax obligations, among other expenses. For those planning an extended stay, perhaps to immerse themselves in local culture or explore specific landmarks like the Golden Gate Bridge or Disneyland, understanding these underlying costs can help manage expectations regarding rental prices.

The system also fosters a sense of stability for long-term homeowners, encouraging them to stay put, which can limit housing inventory in desirable areas. This scarcity further drives up property values and, for new buyers, property taxes, creating a cycle that shapes the availability and affordability of different housing and temporary living options.

Investment Opportunities and Challenges in Hospitality

California’s hospitality sector is a cornerstone of its economy, attracting global brands and independent operators alike. From boutique hotels in Monterey to grand resorts in Lake Tahoe, the state offers diverse investment opportunities. However, property taxes play a significant role in the financial viability of these ventures.

For investors looking to develop new hotels or acquire existing properties, the property tax assessment based on the purchase price is a major operational cost. A newly built Four Seasons Hotel or a newly acquired Ritz-Carlton property will have its property taxes calculated based on its full market value at the time of acquisition or completion. These taxes, along with other operational expenses like payroll, utilities, and marketing for local attractions like Universal Studios Hollywood, must be factored into room rates and revenue projections.

Conversely, established hotels that have not changed ownership in many years may benefit from lower property tax assessments due to Proposition 13’s 2% annual cap. This can provide a competitive advantage in terms of operational costs, potentially allowing for more flexible pricing strategies or higher profit margins. For instance, an iconic Hyatt Regency that has been under the same ownership for decades might have a comparatively lower property tax burden than a brand-new competitor.

Investors also need to be particularly aware of Mello-Roos taxes in newly developed tourist areas or master-planned communities. These special taxes, while funding necessary infrastructure, can significantly elevate the annual property tax bill, impacting the return on investment for new hotels or large-scale resorts. Thorough due diligence regarding all potential assessments is critical before committing to any real estate investment in California’s hospitality sector.

Navigating Property Taxes as a Potential Homeowner or Long-Term Visitor

For individuals contemplating a move to California or considering a long-term rental, understanding the nuances of property taxes extends beyond mere percentages. It involves appreciating regional variations and potential relief programs that can make a substantial difference in the overall cost of living and the feasibility of a desired lifestyle.

Exploring Diverse Regional Rates and Costs

While the 1% base rate is uniform across the state, the effective property tax rate varies significantly from county to county, and even city to city, due to the aforementioned local assessments, bond measures, and Mello-Roos districts. This means that the total property tax on a similarly valued home could be quite different depending on its specific location.

- Higher Rates in Newer Developments: Areas that have undergone significant recent development, often in counties like Riverside County or parts of Orange County, tend to have higher effective tax rates. This is because new infrastructure (roads, schools, utilities) is often funded through Mello-Roos bonds, which add a considerable amount to the property tax bill. If your dream accommodation is a modern home in a master-planned community near Disneyland or Palm Springs, expect to pay a higher effective rate.

- Lower Rates in Established Areas (for long-term owners): Conversely, properties in older, established communities where significant infrastructure is already in place, and that haven’t changed ownership in many years, may enjoy relatively lower effective tax rates. For example, a home in Sacramento that hasn’t sold since the 1980s might have a much lower property tax bill than an identical new build nearby.

- Urban vs. Rural Differences: Major urban centers like Los Angeles and San Francisco often have numerous local bonds for public transportation, schools, and other city services. While property values are exceedingly high, the effective tax rate might still be within the typical 1.1% to 1.3% range, though the absolute tax bill will be substantial due to the high property value. Rural areas might have fewer additional levies, but this depends entirely on local voter-approved initiatives.

For those planning to relocate or seeking a long-term rental, it’s prudent to research the specific tax rates for their desired zip code or community. Real estate listings often provide an estimated annual property tax, which is a good starting point for budgeting.

Exemptions and Relief Programs for Homeowners

California offers a few programs that can help mitigate the property tax burden, primarily for homeowners. While these don’t change the base rate or assessments, they can provide valuable savings.

- Homeowners’ Exemption: The most common relief program is the Homeowners’ Exemption. If you own and occupy a property as your principal place of residence, you can claim an exemption of up to $7,000 off the property’s assessed value. While this might seem modest in a state with high property values, it translates to an annual saving of approximately $70 (1% of $7,000). Every bit counts, and it’s essential for all eligible homeowners to apply for this.

- Exemptions for Seniors, Veterans, and Disabled Persons: California also provides more significant property tax relief programs for specific groups. These include:

- Senior Citizen and Disabled Citizens Property Tax Postponement Program: This allows eligible low-income seniors and disabled individuals to postpone payment of property taxes on their primary residence. The state then holds a lien on the property, and the taxes become due when the property is sold, transferred, or the owner dies.

- Disabled Veterans’ Exemption: This provides a substantial exemption for qualified disabled veterans and their unmarried surviving spouses, significantly reducing their assessed property value.

These exemptions are designed to support vulnerable populations and ensure that property taxes do not become an insurmountable barrier to maintaining a home and a comfortable lifestyle. While these programs primarily benefit full-time residents, understanding them is part of comprehending the broader economic context for those considering making California their permanent home or even a long-term retreat.

The Broader Economic Picture: Tourism, Infrastructure, and Property Tax Revenue

The property tax system in California, while complex, plays a fundamental role in the state’s economic health and its ability to sustain its world-class tourism industry. The revenue generated from property taxes underpins the very infrastructure and public services that enhance the visitor experience and support the local communities where tourists flock.

Funding Public Services and Infrastructure

Property tax revenue is a primary source of funding for local government services, including schools, fire departments, police, parks, and libraries. These services are not just crucial for residents; they also contribute significantly to the appeal and safety of various destinations and attractions. Well-maintained roads facilitate travel to landmarks like Hollywood or Pebble Beach Resorts. Quality public safety ensures peace of mind for visitors exploring city centers or natural wonders. Strong public schools support a skilled local workforce, which in turn serves the hospitality industry, from hotel staff to tourism guides.

Beyond daily services, property taxes, particularly through bond measures and Mello-Roos districts, finance major infrastructure projects. These could be anything from improving transportation networks that connect airports to popular resorts, to upgrading water and sewer systems essential for new hotel developments, or even investing in parks and recreational facilities that enhance the overall lifestyle and attractiveness of a region for both residents and tourists. The seamless experience of visiting iconic California locations is, in part, a testament to the effective deployment of these tax revenues.

Attracting Investment in Hotels and Attractions

The balance between generating sufficient tax revenue for public services and maintaining an attractive investment climate is delicate. While high property values and associated taxes can seem daunting, the stability offered by Proposition 13’s 2% cap on annual increases can be a positive factor for long-term investors. Once a property’s assessed value is set, the predictable, capped growth of the tax bill allows for more accurate financial forecasting, which is crucial for large-scale hotel and resort developments.

Furthermore, the robust infrastructure and high quality of life funded by property taxes help sustain the very appeal of California as a global tourism magnet. World-class airports, efficient public transportation in major cities like San Francisco, well-maintained state parks, and vibrant cultural attractions all contribute to drawing visitors. This, in turn, fuels demand for accommodation and hospitality services, making investments in these sectors more viable despite the initial tax considerations. The presence of well-known landmarks and diverse experiences provides a strong foundation for a thriving tourist economy, generating the revenue needed to support properties and businesses.

In conclusion, while the property tax rate in California might appear intricate at first glance, its foundational principles (1% base rate, 2% annual cap, reassessment upon sale) and additional local levies are designed to fund essential services that enhance both residential lifestyle and the unparalleled travel and tourism experiences the state offers. For anyone contemplating a move, an investment in hotels or accommodation, or simply seeking to understand the Golden State’s economic heartbeat, a clear grasp of this system is indispensable. It’s a system that, for better or worse, continues to define the unique real estate landscape of one of the world’s most desired destinations.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.