California, a land of sun-kissed beaches, towering redwoods, and vibrant metropolitan hubs, beckons millions of travelers, dreamers, and those seeking a quintessential lifestyle. From the iconic landmarks of San Francisco to the glamorous allure of Los Angeles, and the serene beauty of Napa Valley to the adventurous spirit of Lake Tahoe, the Golden State offers an unparalleled array of destinations, attractions, and experiences. For those considering a long-term stay, investing in property, or simply navigating its stunning landscapes, understanding the nuances of life here extends beyond exploring its famous places or indulging in its local culture and food. It also involves preparing for its unique geological realities, particularly the ever-present conversation around earthquakes.

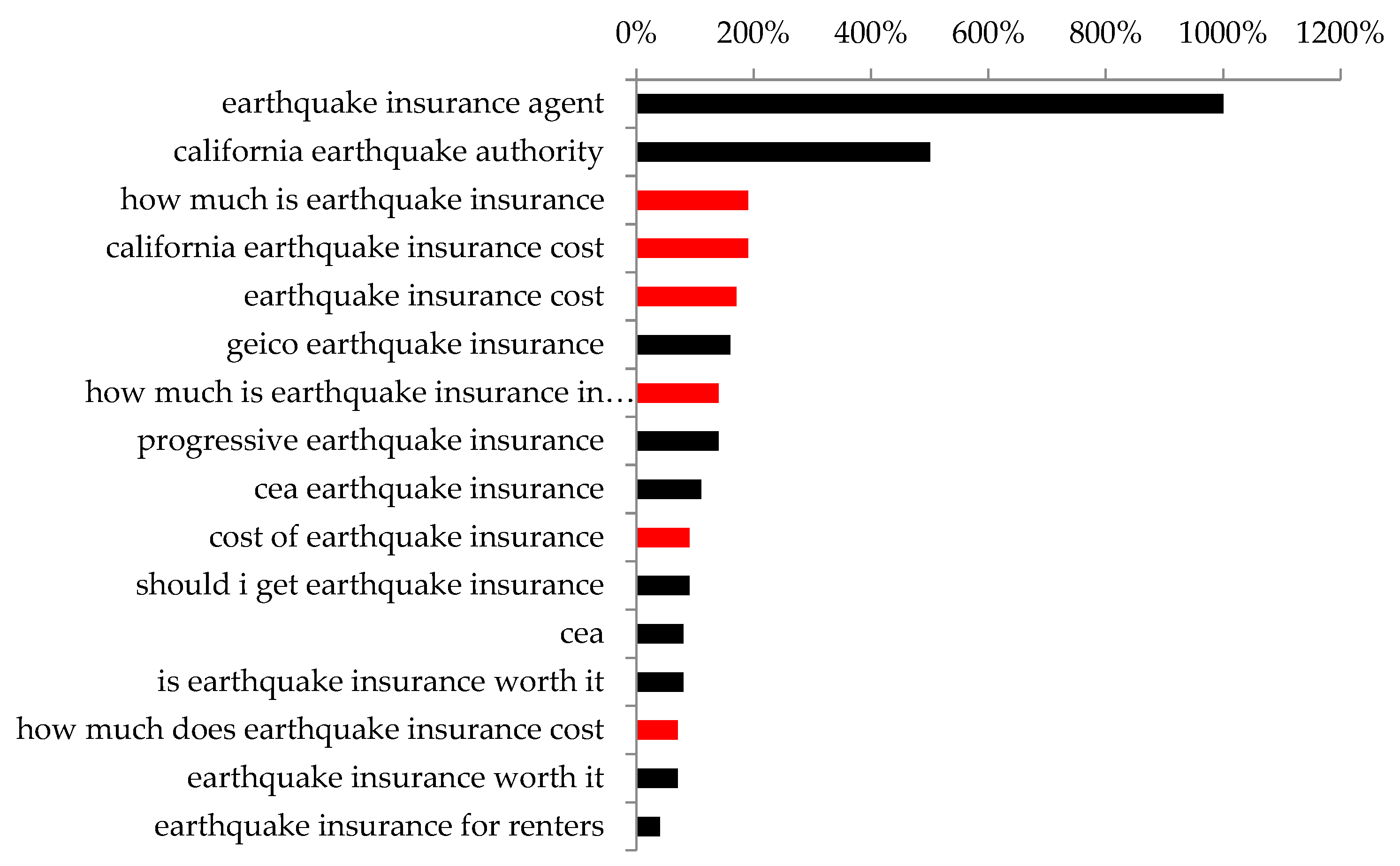

The question “How much is earthquake insurance in California?” isn’t merely about property protection; it’s a critical component of informed living and responsible tourism in a seismically active region. Whether you’re a homeowner, a renter, or even a hotel owner, the potential impact of seismic activity can be substantial. This article delves into the intricacies of earthquake insurance, its costs, and why it’s a vital consideration for anyone embracing the California lifestyle, from luxury travel enthusiasts to those planning budget travel, or families seeking unforgettable trips and businesses establishing their presence. Understanding this aspect of Californian life allows residents and visitors alike to enjoy the state’s wonders with greater peace of mind, ensuring that the dream of California living or an unforgettable vacation isn’t overshadowed by unforeseen events.

Navigating the Golden State’s Tremors: Why Earthquake Insurance Matters for California Life

The allure of California is undeniable, drawing individuals worldwide to its diverse tapestry of landscapes, cultures, and opportunities. For many, it represents the pinnacle of travel, offering everything from world-class resorts and boutique hotels to charming apartments and luxurious villas, catering to every accommodation preference. Its vibrant tourism industry thrives on the promise of unique experiences, whether it’s a walk across the Golden Gate Bridge, the magic of Disneyland Park, or the natural grandeur of Yosemite National Park. However, beneath this picturesque facade lies a geological reality that necessitates a pragmatic approach to personal and property safety: the risk of earthquakes.

While not an everyday concern for most, the occasional tremor serves as a stark reminder of California’s location along the Pacific Ring of Fire, making earthquake preparedness an integral part of living or traveling here. Standard homeowners’ insurance policies, whether for a primary residence, a vacation rental, or a long-term stay accommodation, typically exclude coverage for earthquake damage. This gap in protection means that without a separate earthquake insurance policy, individuals and businesses could face devastating financial losses following a significant seismic event.

For property owners, especially those investing in homes or commercial properties like hotels and resorts, understanding the costs and benefits of earthquake insurance is paramount. It safeguards not only the physical structure but also personal belongings and provides for additional living expenses should a property become uninhabitable. Renters, too, might consider coverage for their personal property. Furthermore, for the broader tourism industry, responsible accommodation providers factor seismic safety and preparedness into their operational plans, enhancing the overall safety and confidence of their guests. The decision to invest in earthquake insurance isn’t just about mitigating risk; it’s about securing the peace of mind necessary to truly embrace the California dream, ensuring that the focus remains on enjoying the state’s unparalleled beauty and vibrant lifestyle.

Understanding California’s Seismic Landscape and Its Implications

California’s breathtaking scenery is a direct result of the powerful geological forces shaping its land. While these forces create majestic mountains and fertile valleys, they also mean the state is crisscrossed by numerous fault lines, making it one of the most seismically active regions in the world. Understanding this landscape is the first step in appreciating why earthquake insurance is such a significant consideration.

The Earth Beneath Our Feet: Major Fault Lines and Historical Context

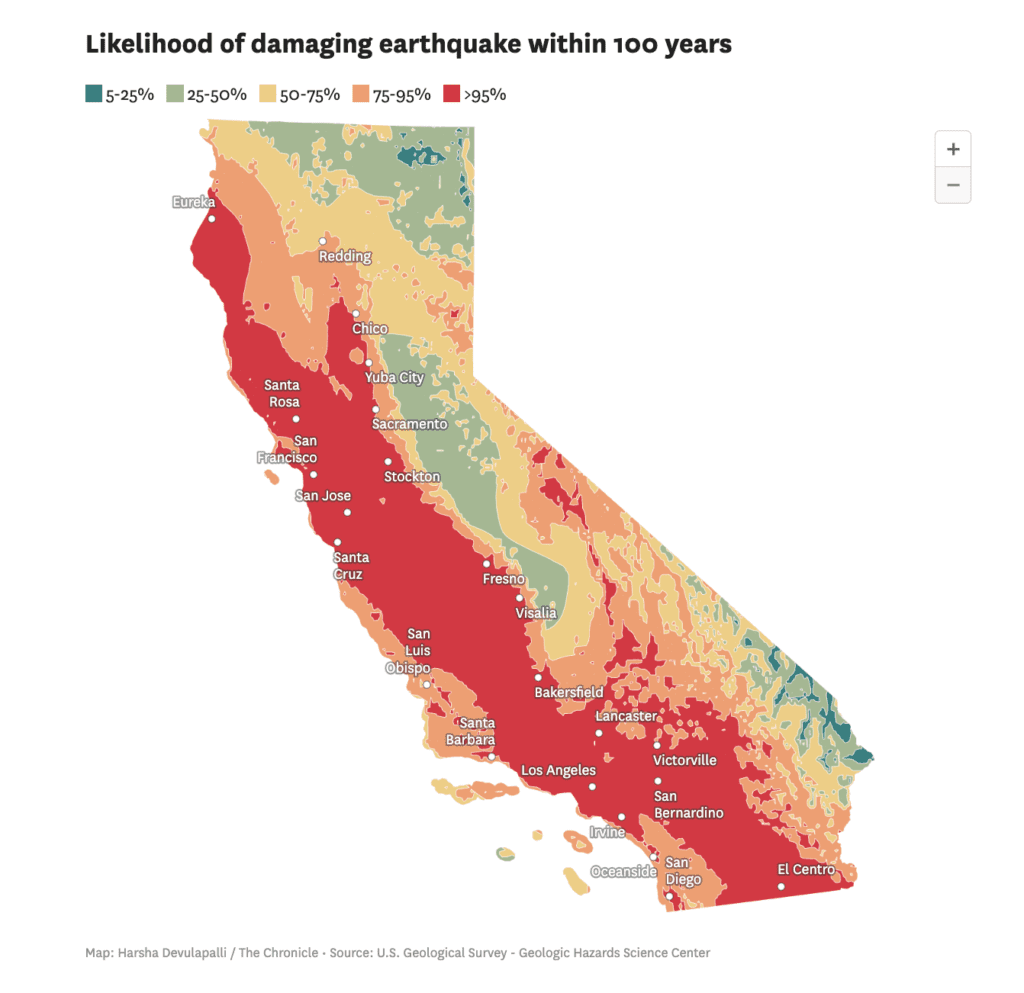

At the heart of California’s seismic activity lies the San Andreas Fault, a massive continental transform fault that runs for approximately 800 miles through the state. It marks the tectonic boundary between the Pacific Plate and the North American Plate, and its movements are responsible for many of California’s earthquakes. Beyond the San Andreas, other significant fault systems exist, such as the Hayward Fault in the San Francisco Bay Area and the Puente Hills Thrust Fault that underlies parts of Los Angeles. These faults, and many others, define seismic hazard zones across the state, with certain areas being at a higher risk of experiencing significant ground shaking.

Historically, California has experienced powerful earthquakes that have reshaped its cities and policies. The 1906 San Francisco earthquake, followed by widespread fires, is a legendary example of the destructive potential. More recent events, such as the 1989 Loma Prieta earthquake and the 1994 Northridge earthquake in Los Angeles, further underscore the need for preparedness and robust infrastructure. These events have not only led to stricter building codes but also highlighted the financial vulnerability of uninsured property owners, reinforcing the demand for specialized earthquake coverage. Cities like Sacramento, while not directly on major fault lines, can still experience shaking from distant quakes, illustrating the widespread nature of the risk.

Beyond Homeowners: The Broader Impact on Tourism and Accommodation

The seismic reality of California isn’t confined to individual homeowners; it has broader implications for the state’s thriving tourism and accommodation sectors. For millions of visitors arriving annually, the safety and resilience of hotels, resorts, and vacation rentals are paramount. Travel guides often highlight iconic landmarks and attractions, but beneath the surface, there’s an expectation of safety and security provided by local infrastructure and businesses.

Hotel chains, independent resorts, and apartment managers catering to long-term stays must adhere to stringent building codes and maintain preparedness plans to protect their guests. The integrity of these structures directly impacts booking confidence and the overall travel experience. A hotel’s ability to withstand seismic activity, or its recovery capabilities post-event, can significantly influence its reputation and future tourism revenue. Similarly, property owners offering villas or suites for rent, whether through luxury travel platforms or budget travel options, bear the responsibility of ensuring their accommodations are as safe as possible.

From a tourism perspective, a major earthquake could temporarily disrupt access to famous places, impact transportation networks, and even alter natural landscapes, affecting everything from guided tours to historical site visits. While such events are rare, their potential to affect the seamless flow of travel and the enjoyment of experiences means that preparedness is an invisible but crucial part of California’s tourism infrastructure. Visitors, while primarily focused on attractions like the Hollywood Walk of Fame or a trip to Alcatraz Island, subconsciously trust in the safety measures undertaken by the state and its businesses. Thus, the conversation around earthquake insurance indirectly supports the broader confidence in California as a premier travel destination, ensuring that visitors can immerse themselves in local culture and activities with peace of mind.

Deconstructing Earthquake Insurance: What It Covers and What Influences Cost

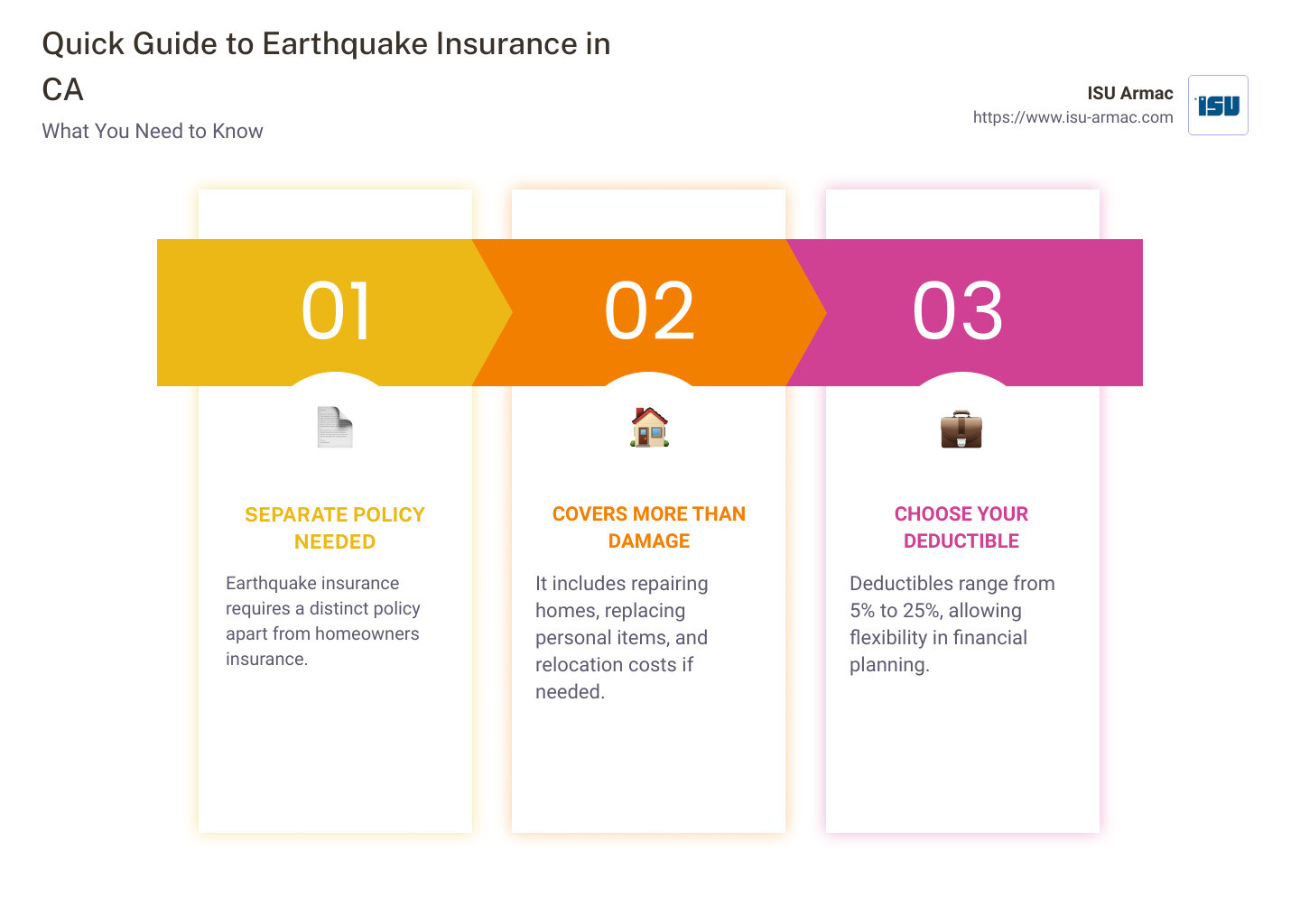

For many, the idea of earthquake insurance can seem complex, an additional layer of protection on top of standard home or business policies. However, understanding its specific purpose and the factors that dictate its cost is crucial for anyone with a stake in California property, from a single-family home to a large hotel. This specialized coverage is designed to address the unique risks posed by seismic activity, distinguishing it from conventional insurance that typically excludes such natural disasters.

What Earthquake Insurance Actually Protects

Unlike standard homeowner’s insurance, which covers perils like fire, theft, and some weather-related damage, earthquake insurance specifically addresses the damage caused by the shaking of the earth. The core components of a policy typically include:

- Dwelling Coverage: This protects the structure of your home or building against earthquake-related damage. For property owners, whether it’s a residential house, an apartment building, or a hotel, this is the most critical component, covering repair or rebuilding costs.

- Personal Property Coverage: This covers the cost of repairing or replacing your belongings inside the damaged dwelling, such as furniture, electronics, and clothing. This is important for homeowners, renters, and even businesses with valuable contents.

- Additional Living Expenses (ALE): Also known as loss of use coverage, ALE helps cover the cost of temporary housing, food, and other essential expenses if your home becomes uninhabitable due to earthquake damage. This is particularly relevant for those seeking long-term stays or operating accommodation businesses, as it ensures continuity for residents or guests.

- Building Code Upgrade Coverage: Some policies offer coverage for the increased cost of repairs due to more stringent building codes enacted after a quake, ensuring the rebuilt structure meets current safety standards.

It’s important to note that earthquake insurance often comes with high deductibles, typically ranging from 10% to 25% of the dwelling coverage limit. This means policyholders are responsible for a significant portion of repair costs before their insurance kicks in. Furthermore, certain damages, like those caused by a subsequent tsunami or fire (which are usually covered by standard home insurance), are often excluded from earthquake policies. Therefore, it’s not a standalone solution but a vital complement to existing coverage.

Key Factors Driving Premiums in the Golden State

The cost of earthquake insurance in California is not uniform; it varies significantly based on several critical factors. These elements are assessed by insurers to determine the level of risk associated with a particular property, directly impacting the premium.

- Location: This is perhaps the most significant factor. Properties located closer to active fault lines, or in areas with a history of high seismic activity, will generally face higher premiums. For example, a home in Oakland, situated near the Hayward Fault, might have a higher premium than a similar property in San Diego, though even San Diego has its own seismic considerations. Insurers use detailed seismic hazard maps to assess ground-shaking potential.

- Property Type and Age: The type of structure (single-family home, condo, apartment, commercial building) and its age play a crucial role. Older homes, especially those built before modern seismic building codes (pre-1980s), are often considered more vulnerable and thus more expensive to insure.

- Construction Materials and Design: The materials used in construction significantly influence resilience. Wood-frame homes generally fare better in earthquakes than unreinforced masonry structures. Properties with specific retrofits, such as bolting the house to its foundation or strengthening cripple walls, may qualify for discounts, as these measures reduce the risk of extensive damage.

- Deductible: As mentioned, deductibles for earthquake insurance are typically high. Opting for a higher deductible will lower your annual premium, but it also means a greater out-of-pocket expense in the event of a claim. Property owners must weigh this trade-off carefully.

- Coverage Limits: The total amount of coverage you purchase for your dwelling and personal property directly affects the premium. More comprehensive coverage, while offering greater protection, will naturally come at a higher cost.

- Insurer: In California, the primary provider of earthquake insurance is the California Earthquake Authority (CEA), a publicly managed but privately funded organization. However, private insurance companies also offer policies, sometimes with different terms, coverage options, and pricing structures. Comparing quotes from both the CEA and private carriers is essential to find the best fit for your needs and budget. For businesses like hotels or resorts, specialized commercial earthquake policies from private insurers might be the only option.

Understanding these factors empowers individuals and businesses to make informed decisions, tailor coverage to their specific needs, and navigate the complex landscape of earthquake insurance in California.

The Numbers Game: Average Costs and Smart Choices for California Living

After delving into the “why” and “what” of earthquake insurance in California, the most pressing question for many remains, “how much?” While exact figures are impossible to provide without specific property details, understanding the typical ranges and how to make smart choices is essential for anyone embracing the California lifestyle, from residents to tourism businesses.

What to Expect: Ballpark Figures and Variances

The cost of earthquake insurance in California can vary widely, typically ranging from $800 to over $3,000 per year for an average single-family home. However, some properties in very high-risk areas or those with substantial value could see premiums extending well beyond this range, potentially reaching several thousand dollars annually.

Here’s a breakdown of how costs might fluctuate:

- Lower End ($800 – $1,500/year): This often applies to newer, wood-frame homes in areas with lower seismic risk (e.g., further from major fault lines, or in regions with less history of severe shaking). Properties that have undergone seismic retrofitting might also fall into this category, as the reduced risk translates to lower premiums. These policies might also feature higher deductibles, further reducing the annual cost.

- Mid-Range ($1,500 – $3,000/year): This is a common range for many homes across California. It includes properties in moderately risky areas, older homes that might not have extensive retrofitting, or those seeking more comprehensive coverage with slightly lower deductibles. Cities like Riverside or Santa Barbara, while beautiful destinations, lie within areas of varying seismic activity, influencing their average costs.

- Higher End (Over $3,000/year): This typically applies to properties in prime seismic hazard zones (e.g., very close to a major fault), older unreinforced masonry buildings, very large or high-value homes, or commercial properties like hotels and resorts. For these larger entities, policies can run significantly higher, reflecting the greater potential for extensive damage and higher rebuild costs. The desire for lower deductibles also pushes premiums into this upper bracket.

It’s crucial to remember that these are just estimates. The specific quote for your property will depend on all the factors previously discussed, including its precise location, construction type, age, desired coverage limits, and chosen deductible. For properties used as accommodation, such as apartments or villas listed for long-term stay or short-term vacation rentals, the cost calculation can also consider the occupancy type and business-related liabilities.

Making an Informed Decision for Your California Journey

Whether you are a long-time resident, a prospective homeowner, or an investor in California’s vibrant tourism and accommodation sector, making an informed decision about earthquake insurance is paramount.

-

For Homeowners and Renters:

- Assess Your Risk: Utilize online tools from the California Earthquake Authority (CEA) or consult local geologists to understand the seismic risk specific to your address. Proximity to active faults greatly influences your vulnerability and premium.

- Get Multiple Quotes: Don’t settle for the first quote. Compare options from the CEA and private insurers. They may offer different packages, deductibles, and coverages. Look for policies that offer coverage for personal property and additional living expenses, which are crucial for maintaining your lifestyle post-quake.

- Consider Retrofitting: Investing in seismic retrofits for older homes can significantly reduce both your risk of damage and your insurance premiums. This is a smart investment in property safety and value.

- Review Your Deductible: Understand the financial implications of your chosen deductible. Can you comfortably cover 10-25% of your home’s value out-of-pocket if a major earthquake occurs?

-

For Travelers and Tourism Businesses:

- Know Your Accommodation’s Preparedness: While individual travelers typically don’t purchase earthquake insurance, choosing hotels, suites, resorts, or apartments that openly demonstrate their commitment to seismic safety and preparedness can offer peace of mind. Reviews often highlight safety aspects.

- Business Continuity: For hotel owners and operators, earthquake insurance is a critical component of business continuity planning. It ensures that post-earthquake repairs can be funded, minimizing downtime and protecting their investment in California’s thriving tourism industry. This reflects a commitment to guest safety and long-term viability.

- Understanding Local Regulations: Businesses offering accommodation for long-term stay or short-term travel should be aware of local building codes and emergency preparedness requirements, which are often stringent in California cities.

Ultimately, earthquake insurance in California is more than just another bill; it’s an investment in resilience. It allows residents to fully enjoy the unique lifestyle offered by this incredible state, from its famous places to its vibrant local culture, knowing they are prepared for its geological realities. For visitors, it underpins the confidence that their travel experiences will be safe, secure, and truly unforgettable, contributing to the Golden State’s enduring appeal as a premier destination for all types of trips.

Conclusion: Securing Your Piece of Paradise

Exploring the costs and considerations of earthquake insurance in California reveals it as an indispensable aspect of life in the Golden State. Far from being an optional luxury, it’s a foundational element of financial security for homeowners, renters, and businesses alike, including those deeply intertwined with the travel, tourism, and accommodation sectors. By understanding the state’s seismic landscape, the specific protections offered, and the factors influencing premiums, residents and visitors can navigate the unique challenges of California with confidence. This preparedness ensures that the dream of experiencing California’s unparalleled destinations, attractions, and vibrant lifestyle can be pursued with peace of mind, allowing everyone to fully embrace the magic of this truly remarkable part of the world.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.