California, the Golden State, has long been synonymous with sunshine, innovation, and an unparalleled lifestyle that attracts millions of visitors and residents alike. From the iconic beaches of Malibu to the bustling streets of San Francisco and the cinematic allure of Los Angeles, the state offers a mosaic of experiences that make it a premier global travel destination. Yet, beneath this vibrant facade, a significant shift is underway that has profound implications for everyone, from homeowners and businesses to the very fabric of its thriving tourism industry: major insurance companies are pulling out or severely limiting their coverage in the state. This exodus isn’t just a business decision; it’s a seismic event that impacts property values, the availability of quality accommodation, and the future of lifestyle within this coveted region of the United States. Understanding why this is happening is crucial for anyone planning a trip, investing in a holiday rental, or simply living the California dream.

A Golden State’ of Shifting Sands: The Core Exodus

The departure of major insurers like State Farm, Allstate, and Farmers Insurance from California is not a sudden, isolated event but rather the culmination of escalating risks and complex regulatory challenges. These companies, which provide essential coverage for homes, businesses, and rental properties, are citing an unsustainable business environment as their primary reason for retreat. The consequences ripple far beyond corporate boardrooms, touching every aspect of life and commerce, including the robust travel and hospitality sectors.

The Escalating Perils: Wildfires and Climate Change

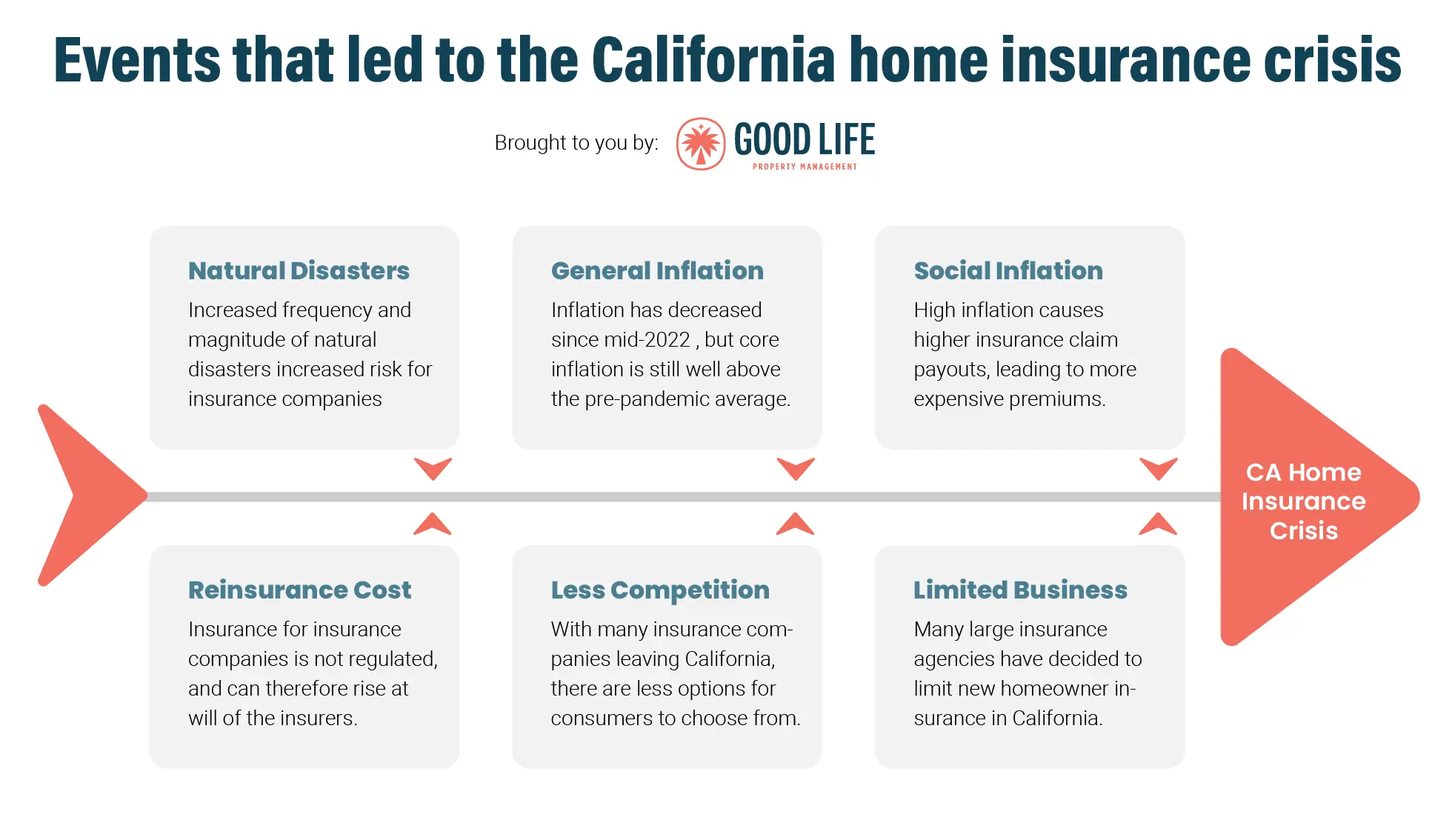

At the heart of the insurance crisis lies California’s increasing vulnerability to natural disasters, particularly wildfires. The state’s unique geography, characterized by sprawling wildlands, dense forests, and dry chaparral, combined with hotter, drier conditions exacerbated by climate change, has created a perfect storm for catastrophic fires. Regions like the Sierra Nevada foothills, parts of Napa Valley, and even suburban areas bordering natural open spaces have become increasingly high-risk zones. The devastation caused by recent wildfire seasons – such as the Camp Fire which decimated the town of Paradise, or the ongoing threats to communities near Lake Tahoe and along the California Coast – has led to billions of dollars in insured losses.

For insurers, accurately pricing risk in such an unpredictable environment becomes incredibly difficult. The frequency and intensity of these events mean that payout costs are skyrocketing, making it challenging to maintain profitability. Even properties far from the immediate fire lines can be affected by smoke damage or increased risk due to proximity to areas designated as high-hazard. This fundamental shift in the risk landscape has forced a reevaluation of traditional underwriting models, leading many companies to conclude that the cost of doing business in California’s most vulnerable areas simply outweighs the potential returns. Beyond wildfires, other climate-related risks like severe droughts, mudslides, and potential seismic activity also contribute to an overall heightened risk profile for the state, further complicating insurance assessments.

Regulatory Hurdles and Business Models

While natural disasters provide the impetus, California’s unique regulatory environment significantly exacerbates the challenge for insurers. The state operates under Proposition 103, enacted in 1988, which gives the elected Insurance Commissioner broad authority to approve rate increases. This regulation aims to protect consumers from excessive rate hikes, but insurers argue it prevents them from charging premiums that adequately reflect the true cost of risk, especially given the escalating natural disaster losses.

Insurers contend that they are unable to factor in forward-looking climate models or catastrophic reinsurance costs – the insurance that insurers buy to protect themselves – when proposing rate increases. They are largely restricted to using historical data, which they argue is no longer sufficient to predict future losses in a rapidly changing climate. This creates a critical imbalance: companies are legally obligated to cover mounting losses but are restricted in their ability to raise premiums to cover those costs or build sufficient reserves. The approval process for rate changes is also often protracted, meaning that by the time an increase is granted, the costs it was meant to cover may have already escalated further. This regulatory framework, coupled with the rising risks, makes California an outlier in the national insurance market, compelling many companies to rethink their long-term strategies in the state. For large international companies, the complex interplay of state-specific rules can be particularly daunting.

Ripple Effects on California’s Tourism and Lifestyle

The retreat of insurance companies is more than a financial headache; it’s a systemic issue that profoundly affects California’s desirability as a place to live, invest, and visit. The connections to the website’s core themes of travel, hotels, tourism, and accommodation become immediately apparent when considering the broader impact.

Impact on Accommodation and Property Values

One of the most immediate and tangible effects is on accommodation – from private residences and vacation rentals to commercial hotels and resorts. Without adequate insurance, securing mortgages or investing in new properties becomes exceedingly difficult. Lenders typically require properties to be fully insured, and if homeowners or developers cannot obtain comprehensive policies, the entire real estate market is destabilized. This can lead to decreased property values in high-risk areas, making it harder for residents to sell or for new buyers to enter the market.

For the travel industry, this presents a unique challenge. Many popular tourist destinations, especially those nestled in scenic, wildland-urban interfaces like parts of Big Sur or areas surrounding Yosemite National Park, rely heavily on vacation rentals and boutique hotels. If property owners in these areas struggle to secure insurance or face exorbitant premiums, some might opt to sell or simply cease operations. This could reduce the availability of unique accommodation options, impacting the diversity of experiences California offers to tourists. Furthermore, the overall perception of risk in owning property could deter investment in new hospitality ventures, potentially slowing the growth of the state’s hotel and resort infrastructure.

Securing Travel and Tourism Investments

Beyond individual properties, the broader infrastructure supporting California’s colossal tourism industry relies on reliable insurance. From theme parks like Disneyland in Anaheim to historic landmarks and natural attractions across the state, operators need comprehensive coverage to protect against various liabilities, property damage, and business interruptions. The cost and availability of these policies directly affect their operating budgets and their ability to plan for the future.

If commercial insurance rates continue to soar or coverage becomes scarce, it could force some businesses to cut back on services, delay expansion, or even face closure. Imagine a charming bed-and-breakfast in a scenic but fire-prone area like Santa Barbara, struggling to afford its insurance premiums. This financial strain could compromise the quality of service, the upkeep of the property, or even its long-term viability. For visitors, this translates to fewer choices, potentially higher prices as businesses pass on increased costs, and a general erosion of the unique local experiences that draw them to California. The vibrancy of events, festivals, and tours – many of which require extensive insurance – could also be affected, diminishing the overall appeal of various destinations.

The Future of Luxury and Lifestyle Travel

California is a mecca for luxury travel, from exclusive retreats in Palm Springs to vineyard stays in Sonoma. The lifestyle associated with these high-end experiences often involves bespoke services, exquisite properties, and a sense of effortless indulgence. The insurance crisis threatens this image and the practicalities of maintaining such operations. High-value properties, whether a Four Seasons resort or a private villa, require extensive and specialized insurance coverage. If this becomes cost-prohibitive or unavailable, it could impact the development and maintenance of these top-tier accommodations.

Wealthy individuals who own multiple properties in California for personal use or as rental investments may find it increasingly difficult to protect their assets. This could lead to a slowdown in the acquisition of high-end homes and a reallocation of investment elsewhere, potentially impacting local economies that thrive on the influx of affluent residents and visitors. The very perception of California as an idyllic, worry-free destination for luxury and leisure could begin to erode if the underlying stability of property ownership and business operation is shaken. For travelers seeking a seamless, worry-free experience, any hint of instability in the local economy or services can influence their destination choices.

Navigating the New Landscape: Tips for Visitors and Residents

Despite the challenges, California remains an unparalleled destination, and steps are being taken to address the insurance crisis. For travelers and those considering a move, understanding the current climate is key to planning effectively.

Planning Your California Travel with Confidence

For tourists, the immediate impact on day-to-day travel is likely minimal. Major hotels and large resorts generally have more robust commercial insurance portfolios and are less directly affected by the residential insurance woes. However, it’s always wise to:

- Book Wisely: When reserving unique accommodation options, especially independent vacation rentals in fire-prone or coastal areas, verify their operational status and reviews.

- Consider Travel Insurance: For significant trips, particularly those involving stays in potentially vulnerable regions, travel insurance that covers unforeseen cancellations or interruptions due to natural disasters can offer peace of mind.

- Stay Informed: Keep an eye on local news regarding wildfire alerts or other natural phenomena, especially during peak seasons. Resources from CalFire and local emergency services are invaluable.

- Support Local: Choose to stay at local establishments and patronize businesses that are working hard to navigate these challenges, contributing directly to the resilience of California’s tourism economy.

Exploring Alternative Solutions and Future Prospects

California is not passively accepting the insurance exodus. The state government, led by the Department of Insurance, is actively engaged in discussions with insurers to find viable solutions. These include exploring reforms to the rate-setting process, promoting mitigation efforts, and potentially developing state-backed insurance programs for high-risk areas. Initiatives like requiring homeowners to harden their homes against fire and offering incentives for doing so are gaining traction. The goal is to create a more stable and predictable market for insurers while ensuring residents and businesses have access to affordable coverage.

For property owners, exploring the state’s FAIR Plan (Fair Access to Insurance Requirements) is a crucial step. This is a state-mandated program designed to be an insurer of last resort for properties unable to obtain conventional coverage. While often more expensive and offering less comprehensive coverage than traditional policies, it provides a crucial safety net. The long-term solution will likely involve a multi-pronged approach: regulatory adjustments, significant investment in climate resilience and mitigation infrastructure, and innovative insurance products that can adapt to changing risks. For example, some insurers are exploring micro-insurance policies or parametric insurance, which pays out based on specific event triggers rather than actual losses, potentially streamlining claims and reducing administrative burdens.

Beyond the Headlines: Preserving the California Dream

The withdrawal of insurance companies from California signals a complex challenge that extends far beyond the financial sector. It highlights the growing tension between evolving environmental realities, consumer protection, and business viability. For a state so deeply intertwined with its natural beauty and outdoor lifestyle, the ability to protect homes, businesses, and public infrastructure against increasingly frequent and intense natural disasters is paramount.

The story of California is one of resilience and innovation. From the tech hubs of Silicon Valley to the agricultural heartland, the state has consistently adapted to new challenges. The current insurance crisis, while daunting, also presents an opportunity to reimagine how communities coexist with nature, how regulations can foster both stability and protection, and how the tourism industry can continue to thrive amidst a changing climate. As discussions continue and solutions are sought, the spirit of the Golden State endures, beckoning travelers to explore its diverse landmarks, indulge in its rich culture, and experience a lifestyle that remains uniquely Californian, even as it navigates a shifting landscape. The future of travel and accommodation in California will undoubtedly reflect these adaptations, ensuring that the state continues to be a world-class destination for generations to come.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.