Florida, often celebrated as the Sunshine State, is a magnet for travelers, retirees, and those seeking a vibrant lifestyle amidst beautiful beaches and world-class attractions. From the magical realm of Walt Disney World Resort in Orlando to the bustling cultural hub of Miami, and the pristine natural beauty of the Florida Keys or Everglades National Park, its appeal is undeniable. However, beneath the allure of its picturesque landscapes and endless activities lies a less glamorous reality for residents and frequent visitors: alarmingly high auto insurance premiums. Many who relocate to or even just frequently visit Florida are often caught off guard by the steep costs of insuring their vehicles, leading them to question why this tropical paradise demands such a premium for basic protection. The answer is a complex tapestry woven from unique demographic factors, environmental challenges, specific state laws, and a litigious local culture, all heavily influenced by its status as a premier global tourism destination. Understanding these contributing factors is crucial for anyone navigating the roads of this dynamic state, whether for a dream vacation or daily life.

The Sunshine State’s Unique Challenges

Florida’s distinctive characteristics, while contributing to its charm and economic vitality, also present significant challenges for the auto insurance industry. The very elements that draw millions to its shores – its rapid growth, diverse population, and vulnerability to natural phenomena – simultaneously escalate the risk for insurers, translating directly into higher costs for consumers.

High Population Density and Tourist Influx

One of the most significant drivers of high auto insurance costs in Florida is its combination of burgeoning resident population and massive tourist numbers. As the third most populous state in the United States, Florida’s major metropolitan areas like Miami, Orlando, Tampa, and Jacksonville experience considerable traffic congestion. This high density of vehicles on the road naturally increases the probability of accidents. More cars mean more opportunities for collisions, even minor fender-benders, each requiring a claim to be filed.

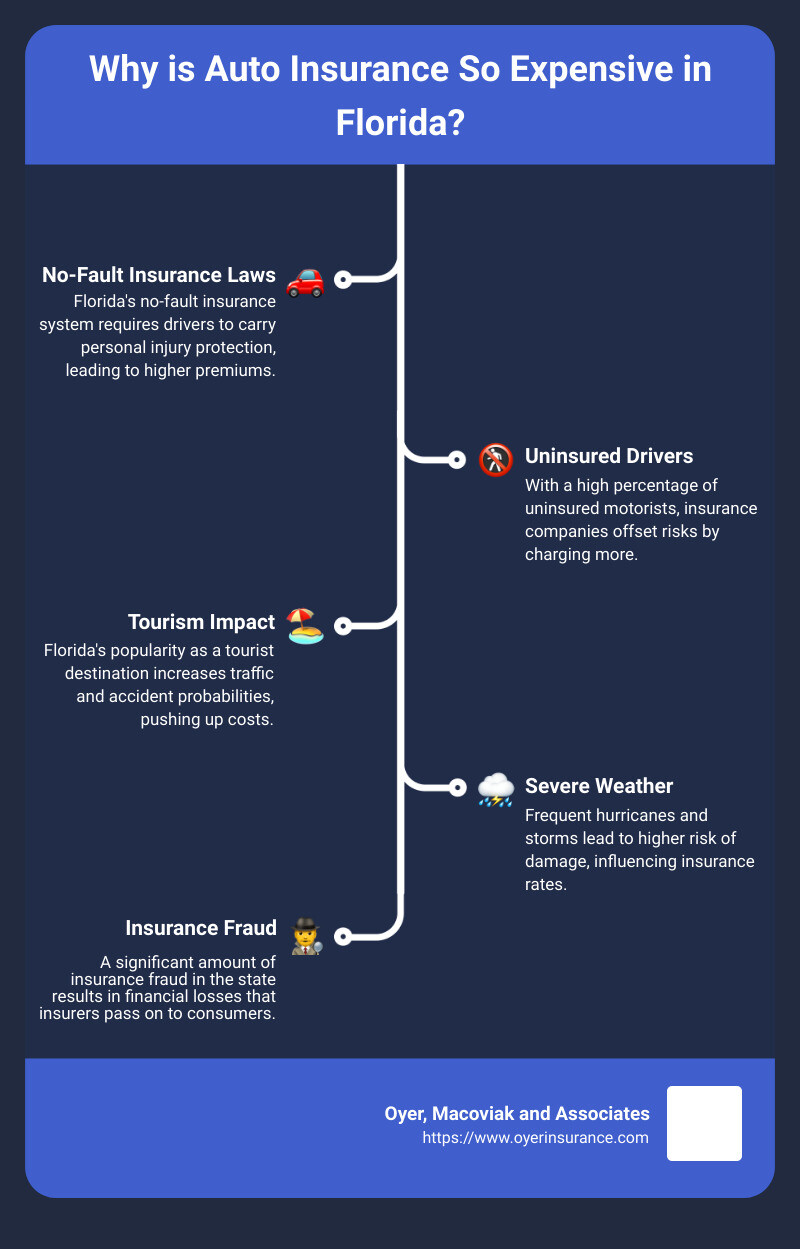

Beyond its permanent residents, Florida welcomes over 130 million tourists annually. These visitors, often unfamiliar with local road networks, traffic laws, or driving habits, contribute significantly to the volume of traffic and the potential for accidents. Many tourists rent cars, adding to the sheer number of vehicles on the roads, especially around popular attractions like Universal Orlando Resort, Busch Gardens Tampa Bay, or the pristine beaches of South Beach. While rental car insurance often covers accidents, the claims still contribute to the overall risk pool within the state, impacting the statistics insurers use to set rates. This constant influx of unfamiliar drivers creates a dynamic and unpredictable driving environment, forcing insurance companies to price in a higher level of risk. The high volume of traffic, particularly in tourist hotspots, leads to an increased frequency of claims, which inevitably pushes premiums upwards for everyone.

Moreover, the state’s transient “snowbird” population, individuals who reside in Florida for part of the year, also complicates risk assessment. Their temporary presence adds to the congestion during peak seasons, and their driving records might be harder to verify consistently across states, potentially leading to higher perceived risk by insurers. The blend of diverse driving experience levels – from seasoned locals to international tourists and seasonal residents – creates a complex risk profile that few other states encounter to the same degree. This kaleidoscope of drivers, all navigating shared roads, elevates the statistical likelihood of incidents, making auto insurance an expensive necessity in the state.

Weather-Related Risks and Natural Disasters

Florida’s geographic location, while perfect for a sun-drenched lifestyle and attracting visitors from colder climates, also places it squarely in the path of severe weather events. The hurricane season, which typically runs from June to November, poses a significant and perennial threat. Major hurricanes and tropical storms, such as Hurricane Irma or Hurricane Ian, can cause widespread damage to vehicles, infrastructure, and property. This damage isn’t just limited to direct impact; flooding, fallen trees, and flying debris during storms can total vehicles or necessitate costly repairs.

In addition to hurricanes, Florida experiences frequent thunderstorms, often accompanied by heavy rain, strong winds, and hail. These conditions can significantly reduce visibility, make roads slick, and contribute to a higher incidence of accidents. Hail damage, while less common than in some other parts of the United States, still occurs and can lead to expensive bodywork claims. Furthermore, the sheer amount of saltwater exposure in coastal areas can accelerate corrosion on vehicles, leading to more frequent mechanical issues that might manifest as claims down the line, even if not directly accident-related.

Insurance companies must factor in the high probability of these natural disasters when calculating premiums. They operate under the assumption that a certain percentage of their policyholders will likely file claims due to storm damage in any given year. The catastrophic nature of hurricanes means that a single event can result in billions of dollars in claims across the state, stretching the resources of insurers and often leading to widespread rate increases to offset these massive payouts. This environmental vulnerability is a fixed cost of doing business in Florida for insurance providers, and it is a cost that is ultimately passed on to the consumer. The state’s beautiful, low-lying coastal areas, while desirable for hotels, resorts, and residential developments, are also the most exposed to storm surge and wind damage, further intensifying the financial risk for vehicle owners and their insurers.

Legal Landscape and Economic Factors

Beyond the environmental and demographic pressures, Florida’s unique legal framework and certain economic realities significantly contribute to the elevated cost of auto insurance. These factors often create an environment where claims are more frequent, more expensive to settle, and more susceptible to fraudulent activity, all of which directly impact the consumer’s wallet.

The Impact of Personal Injury Protection (PIP)

Florida is one of a handful of “no-fault” states, which means it mandates Personal Injury Protection (PIP) coverage. Under the no-fault system, regardless of who caused an accident, your own insurance company pays for your medical expenses and lost wages up to a certain limit (typically $10,000 in Florida). The intention behind PIP is to expedite medical care for accident victims and reduce the number of minor lawsuits clogging the court system. However, in practice, Florida’s PIP system has become a double-edged sword.

While it does provide immediate medical benefits, it has also become a focal point for fraud and abuse. The ease with which minor injuries can be exaggerated and costly treatments prescribed has led to a significant increase in the average cost of claims. This includes scenarios where individuals stage accidents or exaggerate injuries to collect benefits, often in collusion with certain medical providers or attorneys. The system’s design, intended to simplify the claims process, has inadvertently opened avenues for exploitation, leading to inflated medical bills and unnecessary treatments.

Insurers in Florida pay out billions annually in PIP claims, many of which are suspected to be fraudulent or inflated. These rising claim costs, coupled with the administrative expenses of investigating and disputing suspicious claims, are directly passed on to policyholders through higher premiums. Efforts to reform the PIP system have been ongoing for years, with lawmakers struggling to strike a balance between protecting legitimate accident victims and curbing rampant fraud. Until a more robust solution is implemented, the mandatory nature and susceptibility to abuse of PIP coverage will remain a primary driver of Florida’s expensive auto insurance market. For those exploring tourism or considering long-term accommodation in the state, understanding this aspect of the legal landscape is crucial.

A Litigious Environment and Fraud Concerns

Adding to the complexities of PIP, Florida is widely regarded as a very litigious state. This means that after an accident, there’s a higher propensity for individuals to seek legal representation and pursue lawsuits, even for relatively minor incidents. The “bodily injury” component of auto insurance, which covers injuries you cause to others, is particularly impacted by this environment. When an accident leads to a lawsuit, the costs can escalate dramatically due to legal fees, court expenses, and potentially large settlement payouts or jury awards. Insurers must factor in this increased likelihood of legal action and higher settlement costs when setting premiums, especially for bodily injury liability coverage.

The prevalence of “bad faith” lawsuits against insurance companies further exacerbates the problem. These lawsuits allege that an insurer acted improperly by denying or underpaying a claim, and they can result in significant penalties for the insurance company. This pressure often incentivizes insurers to settle claims quickly, even if they suspect exaggeration or fraud, rather than risk a protracted and potentially more expensive “bad faith” lawsuit. This creates a cycle where claims are paid out more liberally, contributing to higher overall costs.

Auto insurance fraud, as mentioned with PIP, is a pervasive issue in Florida. Beyond medical fraud, there are instances of staged accidents, inflated repair estimates, and even individuals filing claims for damages that pre-existed an accident. The state’s transient population, coupled with large urban centers, can sometimes make it easier for fraudulent schemes to operate. Insurers spend substantial resources investigating and fighting these fraudulent claims, but ultimately, the costs associated with both successful and unsuccessful fraud attempts are absorbed into the pricing structure for all policyholders. This combination of a highly litigious culture and persistent fraud concerns creates a challenging environment for insurance companies, directly translating into the steep premiums drivers face across the state. The dynamic nature of Florida’s lifestyle, attracting millions annually, regrettably also provides fertile ground for these detrimental activities.

Understanding Your Options and Mitigation Strategies

While the confluence of factors driving up auto insurance costs in Florida might seem daunting, it doesn’t mean drivers are entirely powerless. Understanding the specific elements that influence individual premiums and knowing how to navigate the market can help mitigate these high costs. By taking proactive steps and making informed choices, residents and frequent visitors can often find ways to manage their insurance expenses more effectively.

Factors Influencing Individual Premiums

Even within Florida’s high-cost environment, individual auto insurance premiums can vary significantly based on several personal factors. Understanding these can help you identify areas where you might be able to save:

- Driving Record: This is arguably the most critical factor. A clean driving record, free of accidents, speeding tickets, or other violations, will always result in lower premiums. Conversely, even a single at-fault accident or a major moving violation can significantly increase your rates for several years. For those who frequently drive between Florida and other states, maintaining a consistent, good record across all jurisdictions is paramount.

- Vehicle Type: The make, model, year, and safety features of your car play a substantial role. Expensive luxury vehicles, sports cars, or those with high theft rates will cost more to insure due to higher repair costs and increased risk. Vehicles with advanced safety features (like automatic emergency braking or lane-keeping assist) might qualify for discounts, as they reduce the likelihood of accidents. Electric vehicles and hybrids, while environmentally friendly, can sometimes have higher repair costs due to specialized components, impacting their insurance rates.

- Location: Even within Florida, your specific zip code matters. Urban areas like Miami or Orlando with higher traffic density, crime rates (especially auto theft), and accident frequencies will typically have higher premiums than more rural or suburban locales. If you’re considering a move or purchasing property for long-term stay, checking insurance rates for the area can be a wise financial move.

- Credit Score: In Florida, as in many other states, insurance companies often use a credit-based insurance score as a factor in determining premiums. Studies have shown a correlation between higher credit scores and a lower likelihood of filing claims. Maintaining a good credit history can therefore indirectly contribute to lower insurance costs.

- Age and Experience: Younger, less experienced drivers, particularly teenagers, are statistically more prone to accidents, leading to significantly higher premiums. As drivers gain experience and mature, their rates tend to decrease, assuming they maintain a good driving record. This also applies to those new to driving in Florida itself, as unfamiliarity with local roads or traffic patterns can be seen as an increased risk.

- Coverage Limits and Deductibles: The amount of coverage you choose (e.g., higher liability limits, comprehensive, collision) and your deductible amounts directly impact your premium. Opting for higher deductibles (the amount you pay out-of-pocket before insurance kicks in) can lower your premium, but means you’ll pay more upfront in the event of a claim. It’s a balance between affordability and financial preparedness.

Navigating Insurance in a High-Cost State

Given the inherent expenses, proactive strategies are essential for securing the most favorable auto insurance rates in Florida. It requires a diligent approach to comparison shopping and a clear understanding of available discounts.

- Shop Around Extensively: Never settle for the first quote. Insurance rates can vary dramatically between different providers for the exact same coverage. Obtain quotes from multiple insurance companies – national carriers, regional providers, and even local independent agents who can access various underwriters. Use online comparison tools and dedicate time to this process. This due diligence is perhaps the most effective way to find competitive pricing in a high-cost market like Florida.

- Bundle Policies: If you have other insurance needs, such as homeowners, renters, or even boat insurance (popular in Florida), inquire about bundling them with the same provider. Many companies offer significant discounts for combining multiple policies, a strategy that aligns well with the diverse lifestyle options available in the state, from city apartments to coastal villas.

- Inquire About Discounts: Don’t hesitate to ask about every possible discount. Common ones include:

- Multi-car discount: For insuring more than one vehicle.

- Good student discount: For young drivers maintaining high academic performance.

- Defensive driving course discount: Completing an approved safety course.

- Low mileage discount: If you drive less than a certain number of miles annually, perfect for those enjoying a more relaxed pace or using public transport more frequently during tourism season.

- Anti-theft device discount: For vehicles equipped with alarms or tracking systems.

- Loyalty discount: For staying with the same insurer for an extended period.

- Occupational or affinity discounts: Some employers or professional organizations have partnerships with insurers.

- Review Coverage Annually: Your insurance needs can change. As your car ages, you might consider dropping comprehensive and collision coverage if its value no longer justifies the premium. Reassess your liability limits as your assets change. An annual review ensures you’re not overpaying for coverage you no longer need or are adequately protected for your current circumstances.

- Maintain a Good Credit Score: As noted, a strong credit score can lead to lower premiums. Regularly check your credit report for errors and work to improve your score if needed.

- Increase Deductibles (with caution): While a higher deductible can lower your premium, ensure you have enough savings to cover that deductible if you need to file a claim. This is a calculated risk that must align with your financial comfort level.

- Consider Telematics Programs: Many insurers offer programs that monitor your driving habits (speed, braking, mileage) via a smartphone app or a device plugged into your car. Safe drivers can earn significant discounts through these programs, providing a direct way to demonstrate responsible driving and potentially offset some of Florida’s systemic high costs.

By understanding the underlying reasons for Florida’s expensive auto insurance and proactively managing personal factors and coverage choices, drivers can navigate this challenging market more effectively. While the state’s unique blend of natural beauty, bustling tourism, and legal intricacies will likely keep premiums elevated, informed consumers have the tools to make the best possible financial decisions for their vehicle protection.

LifeOutOfTheBox is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.